In recent years, China’s humanoid robot industry has developed rapidly: it started in 2023, accelerated its expansion in 2024, gradually took root in 2025, and entered a period of reshuffling in 2026.

Behind these changes, the hand of policy is almost ubiquitous.

From the national to the local level, various special funds, industrial plans, and innovation programs have been continuously introduced; some cities have established special task forces to practically bring humanoid robot companies to their doorsteps, and have even built innovation centers and training grounds to provide companies with real-world application scenarios; state-owned asset platforms and local funds have become frequent clients for corporate financing.

As a result, many companies have focused their attention on government and public platforms: seeking investment, building experimental fields, and promoting implementation… some have even stated explicitly, “To implement, you must buy my robots.” In a short period, “to G” has almost become the natural path for the humanoid robot industry.

But the question is, what will happen if this path continues in the long run? When the government becomes the main customer, and when application scenarios heavily rely on policy and financial support, can companies establish themselves in a broader market? This is precisely the core dilemma faced by many humanoid robot companies.

- The Secret to Rapid Enterprise Deployment: Government Funding

For the domestic humanoid robot industry, policy is the most prominent safeguard.

At the central level, in 2023, the Ministry of Industry and Information Technology issued the Guiding Opinions on the Innovative Development of Humanoid Robots, establishing the underlying logic and roadmap for industry development. Between 2024 and 2026, policy support went beyond top-level guidance, gradually expanding to standard setting, market cultivation, and industry standardization.

While there is top-level design at the national level, local governments have also introduced supporting measures: some provinces and cities have built robot innovation centers and training grounds, established special funds to attract talent and enterprises, and promoted the implementation and operation of various experimental platforms and application demonstration scenarios; other cities have included robotics in their key industrial development priorities, guiding local universities, research institutions, and manufacturing enterprises to collaborate.

According to statistics from Humanoid Robot Scene Application Alliance (HRAA), as of March 2026, more than 50 humanoid robot data collection centers/training grounds and more than 20 humanoid robot and embodied intelligence innovation centers have been built across the country, and the number continues to grow.

These policy packages and significant investments have naturally shaped the industry’s implementation path. A large amount of capital has flowed to humanoid robot companies through state-owned asset platforms and industry guidance funds. Government procurement, training base construction, and public service scenarios have become among the easiest areas for implementation.

For companies, where there are money, scenarios, and data sources, there will be the first places to test and validate their products.

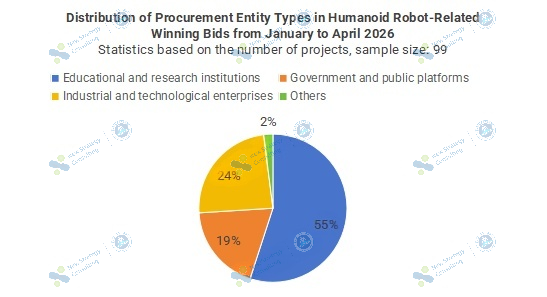

According to statistics from HRAA, in relevant winning bids in 2025 and 2026, universities and vocational schools consistently accounted for the highest proportion, while the proportion of government and public service platforms gradually increased. This data reflects not only that “implementation” is becoming a reality, but also that policy resources are driving the entire industry to accumulate scale and experience first from the “public sector.”

In this context, many companies have focused their strategic efforts on the “to G” market: seeking local government funding and state-owned asset platform investment on the one hand, and collaborating with the government to build laboratories and training grounds to obtain substantial implementation scenarios on the other. Some companies have even downplayed their market-oriented operational capabilities, making obtaining government projects their primary growth path.

It can be said that, driven by policy, the industry has gained momentum and opportunities for implementation in a short period of time. However, this “public sector priority” approach is also quietly reshaping corporate strategic choices, making the logic of “selling to the government guarantees implementation” a default mindset for many startups.

- How Far Can Companies Go under the “toG” Model?

With policy support, “to G” has almost become a natural implementation path for Chinese humanoid robot companies.

The advantages of this path are obvious: stability, predictability, and abundant resources. Universities, vocational schools, and public service platforms become “testing grounds” for companies. Robots iterate continuously in these scenarios, allowing companies to verify technology, optimize functions, and improve reliability using real data. At the same time, the participation of state-owned capital and local funds reduces early-stage R&D risks, giving startups more space to explore technology.

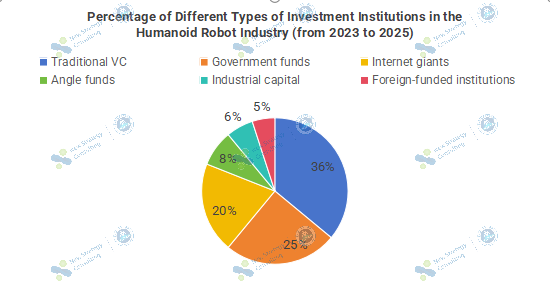

Government funds accounted for 25% of investment in the humanoid robot field from 2023 to 2025

However, behind the benefits, there are also obvious drawbacks. The most obvious is dependency. Once companies become accustomed to the “selling to the government guarantees implementation” model, their business perspective tends to narrow. Changes in policy pace, funding allocation, and procurement plans can jeopardize a company’s survival. While short-term orders may be stable, long-term strategic flexibility is hampered.

Furthermore, the “to G” model imposes implicit constraints on product and technological innovation. Public sector demands are typically concentrated in education, training, or specific service scenarios, naturally leading companies to prioritize these functionalities. This easily results in product homogenization, a lack of focus on a single application scenario, and a lack of innovation for broader markets such as households, retail, or entertainment. In other words, a company may achieve high quality in public sectors, but it hasn’t yet developed true competitiveness in the mass market.

Real-world examples illustrate this: some companies, when building experimental platforms, lock their own robots into the sole solution, gaining orders and exposure in the short term. However, in the long run, this strategy makes them passive in exploring B2B and B2C markets and business models. Once policy direction shifts or market demand changes, these companies must find new growth points, incurring high costs and risks.

Overall, the “to G” model is an engine for rapid industry implementation, but this engine risks overheating. It helps companies accumulate experience and validate technologies, but it can also lead to overly singular strategic choices and weak innovation motivation. To go further in the future, relying solely on policies and public projects is clearly insufficient; market-oriented and diversified capabilities will be key to who stays in the race.

- Breaking Free from “toG” Dependence and Moving Towards Diversified Markets

Currently, many humanoid robot companies in China have realized that relying solely on “to G” is insufficient to support long-term growth. The truly promising path lies in extending to “to B” and “to C.” However, in practice, this path is more complex and realistic than imagined.

In terms of to B, manufacturing and logistics are the most frequently mentioned application scenarios. According to statistics from HRAA, by 2026, more than 30 companies in China had deployed humanoid robots in factories for basic positions such as handling, sorting, loading and unloading, and inspection.

Image: ROBOTERA robots are deployed at the Guangzhou Post Office Center

However, reality is more complex than the numbers. On the one hand, humanoid robots in factories can indeed perform some repetitive and unfriendly tasks, such as material handling and quality inspection; on the other hand, compared to traditional industrial automation systems, humanoid robots still lag behind in stability, efficiency, and cost.

Many companies ultimately choose to pilot these robots in labor-intensive or insufficiently standardized processes, and there is still a long way to go before they can widely replace human labor like robotic arms.

As for to C, some companies are also venturing into family companionship and entertainment. For example, they have launched pre-sales of concept products using robots for early childhood education and home care, attracting some attention and user interest.

However, the practical problem that quickly arises is that family users are more price-sensitive and have much higher expectations for interactive experiences, intelligent understanding, and personalized content than imagined. In other words, simply relying on a “cool appearance” is insufficient to maintain the purchasing power of consumer users.

These cases illustrate that even companies with relatively mature technological foundations still face significant challenges in both the “to B” and “to C” markets: How to integrate robots from government scenarios into the operational rhythms of business clients? How to convince end-users to pay for robots, rather than viewing them as gimmicks? How to find a balance among cost, performance, and user experience?

This doesn’t mean that “diversification” is wishful thinking, but rather that this path requires more solid product and business logic. In the B2B sector, companies need to improve their products’ ability to replace traditional industrial automation equipment and integrate with existing systems; in the B2C sector, they need to explore lower-barrier price ranges, modular service combinations, or subscription services to enhance long-term user retention and willingness to pay.

Industry development itself is a process of shifting from policy-driven to market-driven. Currently, “to G” policies have provided humanoid robot companies with their first pot of capital, their first batch of customers, and their first round of data samples. However, whether they can enter a broader market in the future depends on whether companies can resolve the contradictions between efficiency, cost, and user value in practical applications. This process may be full of iterations and trial and error, but it is far closer to the truth of the market than simply developing products based on policy.

Conclusion:

While policies have provided a starting point for the humanoid robot industry, the real race lies in multi-scenario implementation and market expansion. Companies shouldn’t wait for opportunities but proactively develop B2B and B2C scenarios, building a complete closed loop of products, services, and applications to ensure tangible technological implementation and sustainable market growth.

To promote industry exchange and practical application, the “Closed-Loop Pathfinding, Tangible Implementation: Embodied Intelligence Scenario Private Board Meeting” will be held in Hangzhou on June 24, 2026, to jointly explore the application paths of embodied AI in more scenarios.

Following this, on June 25, the “3rd Embodied Humanoid Robot Scenario Application Expansion Conference 2026” will be held in Hangzhou, bringing together top industry experts, leading scenario providers, and benchmark companies to showcase the latest technologies and implementation cases.