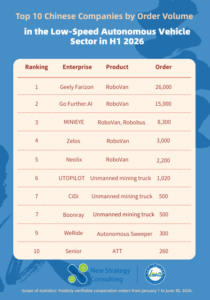

On June 23, Low-speed Automated Driving Industry Alliance (LSAD) learned that “Bamboo Robovan”—an independently operated entity under MINIEYE focused on unmanned logistics vehicles—is nearing the completion of a new round of dedicated, independent financing. The post-investment valuation has reached hundreds of millions of dollars, with investors including top-tier capital from the autonomous driving industry.

Previously, it was revealed that WeRide also planned to spin off its Robovan division for independent financing, targeting a valuation of $400 million.

With MINIEYE and WeRide making similar moves in succession, is this merely a coincidence, or a signal that the valuation logic of the autonomous driving industry is undergoing a fundamental shift?

The Rise of the Autonomous Driving “Spin-off Wave”

LSAD has found that there are many similar examples of capital restructuring within the autonomous driving sector.

For instance, to engage more flexibly with automakers or logistics industry capital, DJI spun off its automotive business into an independent entity, ClixPilot, in 2023. This move not only secured a strategic investment of over RMB 3.6 billion from FAW Group—rapidly pushing its valuation past the RMB 10 billion mark—but also set the company on the path to an independent IPO.

Pony.ai has long operated and sought financing for its Robotruck and Robotaxi businesses under independent structures. This strategy aims to align with capital sources possessing varying risk appetites and to insulate logistics deployment operations from the R&D risks associated with “long-tail” driving scenarios.

Baidu Apollo also bundled its robotaxi service, Apollo Go, with its Apollo technology foundation to form an independent autonomous driving company. This move was designed to break free from the valuation framework associated with Baidu’s “traditional search advertising” business, allowing for independent capital market valuations based on the specific “hard tech” sectors to which each business belongs, thereby unlocking and highlighting the true value of these assets.

Similarly, Horizon Robotics—a company deeply rooted in ADAS solutions—spun off its robotics computing platform business (a non-core automotive operation) in late 2024 to establish an independent company named D-Robotics, which subsequently raised its own capital.

From MINIEYE and WeRide to DJI, Pony.ai, and Baidu, this series of events represents a collective strategic restructuring of business architectures and valuation models by leading companies as the autonomous driving industry enters the “deep water zone” of commercialization.

Why Are Major Players Collectively “Splitting Up”?

At the same time, we can discern the logic driving these capital maneuvers:

From a subjective standpoint, the primary goal is to break the “all-suffer-together” valuation discount applied to the business as a whole. Amidst tightening liquidity in the primary market and valuation pressures in the secondary market, the old model of bundling diverse businesses for a single valuation has become increasingly ineffective. Long-cycle, high-loss operations often drag down the valuation multiples of businesses that possess clear commercialization paths and stable cash flow projections.

By spinning off autonomous driving units—as seen with companies like MINIEYE, WeRide, and DJI—enterprises can shed the loss-making burdens of the parent company. This allows high-quality assets to be valued independently based on the logic applied to “hard tech,” unlocking hidden asset value, injecting much-needed liquidity into the parent company, and optimizing the group’s overall PE/PB ratios.

Secondly, spin-offs optimize capital alignment and resource synergy. Different business lines have distinct requirements regarding capital characteristics and resource endowments. In the autonomous driving sector, for instance, Robotaxi operations represent a classic long-cycle venture investment requiring high risk tolerance and sustained capital backing; conversely, Robovan businesses align better with the priorities of industrial capital, focusing on order certainty, cost-reduction ROI, and payback periods. Independent spin-offs allow for greater flexibility in attracting capital and facilitate the use of equity ties to secure specific use cases and orders, thereby creating a “technology-plus-scenario” partnership of shared interests.

From an objective perspective, spin–off is an inevitable choice for revitalizing organizational vitality as competition shifts to a more intense, complex level.

As competition in the autonomous driving industry enters a critical, high-stakes phase, technological barriers and deployment efficiency have become the decisive factors. For industry leaders with deep technical foundations—such as MINIEYE, DJI, and Baidu—spinning off mature businesses serves the core purpose of shedding the “big corporate” bureaucracy. Under a traditional group structure, emerging autonomous driving units often face marginalization in resource allocation and sluggish decision-making processes. Furthermore, within such vast corporate systems, core technical personnel often struggle to secure equity incentives commensurate with their contributions, leading to a risk of talent attrition.

By operating and raising capital independently, these business units can concentrate strategic resources, respond agilely to market demands, rapidly iterate products, and accelerate deployment.

Conclusion:

MINIEYE’s decision to spin off its Robovan business for independent valuation and financing is not merely a tactical move to optimize capital structure and establish a second growth curve; it also validates the feasibility of the strategy where “passenger-vehicle-grade intelligent driving technology disrupts low-speed application scenarios.” For the industry, the collective move by leading players—such as Bamboo Robovan and WeRide Robovan—to spin off and seek independent financing signals that asset operations are becoming increasingly refined and mature. It marks the entry of the low-speed autonomous driving sector into a phase where commercial viability and closed-loop business models are the primary drivers of value realization.

At the same time, this wave of spin-offs will accelerate industry consolidation, compelling companies to shift their focus from merely competing on technical demonstrations to rigorously pursuing profitable business models, efficient supply chain integration, and deep ecosystem development. A company’s ability to generate its own revenue—its “self-sustaining capability”—will be the key metric for evaluation in the next stage.

Against this backdrop, collaborative innovation within the industrial ecosystem has become crucial. As the industry navigates a critical window of rapid technological iteration and business model restructuring, integrating upstream and downstream resources while exploring pathways for sustainable, large-scale deployment is a challenge shared by all stakeholders.

To address this, the 6th Low-Speed Autonomous Driving Scenario Ecosystem Co-construction and Expansion Conference 2026 will be held by LSAD from July 23 to 24, 2026, at the Sheraton Hefei Xinzhan Hotel. The event will bring together OEMs, solution providers, end-users, and key industry representatives to deeply explore the critical path from pilot validation to large-scale commercialization and to envision the future of unmanned operations.

We look forward to the participation of more innovative enterprises possessing core technological strengths, as we work together to propel China’s low-speed autonomous driving industry into a new stage of high-quality development through ecosystem synergy.