Looking back at the industrial evolution of mobile robotics, the manufacturing process has always served as the core foundation for enterprises to achieve large-scale replication, ensure delivery reliability, and implement technological solutions. Particularly during the critical transition from China’s manufacturing sector to China’s intelligent manufacturing, mobile robotics—as representatives of smart equipment—see their manufacturing capabilities upgraded. This advancement not only enhances corporate competitiveness but also serves as the cornerstone supporting the intelligent transformation across various industries.

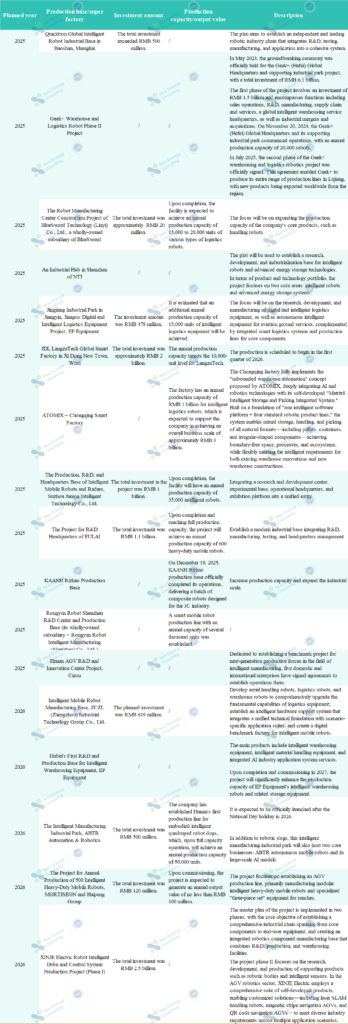

Since 2025, the mobile robotics industry has witnessed a wave of intensive factory construction, production launches, and capacity expansions. According to statistics from China Mobile Robot Industry Alliance (CMRA) and New Strategy Mobile Robot Industry Research Institute (NSRI), from 2025 to March 2026, more than 16 mobile robotics-related companies announced plans for factory construction, production expansion, or commissioning, with cumulative investments exceeding RMB 9 billion. Among the projects that disclosed investment amounts, five involved single investments exceeding RMB 1 billion.

This figure not only reflects an unprecedented surge in market confidence within the industry, but also epitomizes enterprises’ strategic determination to accelerate the positioning of their manufacturing capabilities.

I. Accelerated Expansion: A Wave of Growth sweeps Across China Throughout the Year

Throughout 2025, the pace of factory construction in the mobile robotics industry continued to accelerate. From the signing of the Phase II project for Geek+’s Hefei headquarters and supporting industrial park, to the commencement of construction on the BlueSword Manufacturing Center, and further to the launch of the Cizon Hunan AGV R&D and Innovation Center project—the factory construction and commissioning have evolved from a strategic initiative into a year-round industry norm.

After entering 2026, the momentum of production expansion not only persisted but intensified further. Within just three months of 2026, multiple mobile robot projects with investments exceeding RMB 500 million were successively launched. In January, ZCZL invested RMB 619 million to establish an intelligent mobile robot manufacturing base; in February, EP Equipment’s first intelligent warehousing equipment R&D and production base in Hubei officially commenced construction; in March, the joint investment project between MORTISEON and Haipeng Group for producing 500 intelligent heavy-duty mobile robots per year was formally signed and implemented. The investment scale and strategic scope of each project saw significant increases compared to the previous year.

Behind this series of intensive developments lies not only a clear delineation of the evolving competitive landscape in the mobile robotics industry, but also reveals the underlying demand dynamics and strategic intentions driving corporate strategic positioning.

Chart 1: Progress of Factory Construction and Production Expansion in Chinese Mobile Robotics Sector from 2025 to March 2026 (Compiled by CMRA Based on Publicly Available Data)

Throughout this wave of production expansion spanning 2025 to 2026, the most striking change is the exponential growth in investment scale, marking the industry’s entry into a new phase.

During this period, JDL LangzuTech invested a total of RMB 2 billion in its global smart factory; Suzhou Junion Intelligent Technology Co., Ltd. Invested RMB 1 billion in its smart mobile robot and radar production, R&D, and headquarters base project; EULAI invested RMB 1.1 billion in its R&D headquarters project; and XINJE Electric’s robot intelligent drive and control system production project (Phase I) reached a total investment of RMB 2.5 billion. Frequent emergence of “RMB 1-billion-plus” investment projects has completely shattered the previous industry expansion pattern characterized by light asset intensity, signaling that mobile robot manufacturing capacity development has officially entered a new phase marked by heavy asset investment and a broader strategic framework.

From the perspective of industry participants, the wave of production expansion vividly demonstrates the appeal of this sector. Beyond specialized mobile robotics companies, system integrators like NTI and internet giants such as JDL have also entered the field, with their commitment to this area growing steadily. A prime example is JDL LangzuTech Global Smart Factory in Wuxi Xi Dong New Town, which requires a total investment of RMB 2 billion—a hallmark case of internet giants making substantial investments in strategic positioning.

Core component manufacturers are expanding vertically, system integrators are growing horizontally, and internet giants are making substantial investments across industries. This diversified corporate landscape directly reflects the continuously rising attractiveness of the sector. Competition in the mobile robotics industry has evolved from mere “product comparisons” to a comprehensive “systematic contest of full-stack capabilities.”

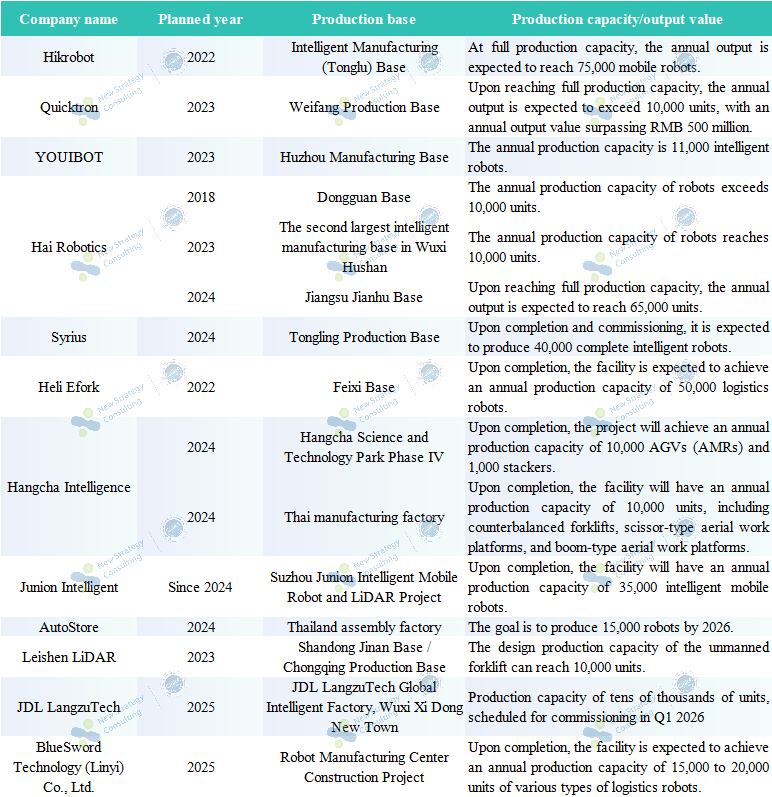

Meanwhile, as foundational capabilities in intelligent manufacturing continue to improve and market demand rapidly expands, numerous mobile robot production bases with annual capacities exceeding 1,000 units—or even reaching the tens of thousands—have been rapidly established. The ‘super factory’ concept has evolved from a forward-looking initiative by individual enterprises into a collective effort driving industry advancement, with the ranks of super factories steadily growing.

From the perspective of production base capacity planning, enterprises ‘strategic layout decisions are becoming increasingly evident. The robot manufacturing center built by BlueSword Technology (Linyi) Co., Ltd., a wholly-owned subsidiary of BlueSword, is expected to produce 15,000 to 20,000 units of various logistics robots annually upon completion; JDL smart factory in Wuxi Xi Dong New Town aims for an annual production capacity of tens of thousands of units; the smart mobile robot and radar production, R&D, and headquarters base of Suzhou Junion Intelligent Technology Co., Ltd. will achieve an annual output of 35,000 intelligent robots upon completion. Additionally, companies such as ABTR Automation & Robotics have also clarified their respective production capacity plans, striving to establish core competitive advantages through enhanced manufacturing capabilities.

This round of production capacity planning vividly reflects the industry’s strong expectations for market growth, as well as companies’ strategic determination to accelerate market share acquisition and build competitive moats through capacity expansion.

II. The Wave of Production Expansion: A Close Look at the Five Key Drivers

Behind this series of production expansion and factory construction initiatives, five core motivations clearly emerge. These factors collectively drive comprehensive development in the mobile robotics industry during the expansion process, enabling companies to secure a competitive edge in the highly competitive market.

The primary demand stems from the practical pressures of rising market demand and shortened project delivery cycles. The deep integration of manufacturing automation upgrades and smart logistics has driven rapid growth in mobile robot orders, with delivery pressures directly impacting manufacturing operations. Those capable of delivering large volumes of products reliably within shorter timeframes gain a competitive edge in bidding. EP Equipment’s digital and intelligent logistics equipment project in the Jingjiang Industrial Park aims to increase annual production capacity by 15,000 units, while ATOMIX’s Chongqing factory is positioned to support the company’s business scale of approximately RMB 3 billion. These expansion initiatives represent direct responses to genuine delivery demands.

Meanwhile, the capacity race among “super factories” is accelerating. Production capacities in the tens of thousands of units are evolving from industry top-tier specifications to standard configurations. The Hikrobot Intelligent Manufacturing Base (Tonglu) aims to achieve an annual output of 75,000 mobile robots upon full production capacity; the Hai Robotics Innovation Jiangsu Jianhu Base is projected to produce 65,000 units annually; and the AutoStore Thailand assembly plant is expected to manufacture 15,000 robots by 2026. This collective surge in production capacity figures vividly reflects the industry’s strong expectations for market growth and companies’ strategic determination to accelerate market share acquisition.

Chart: Production Capacity/Output Value of Mobile Robot Projects with Partial Production Capacity at the Ten-Thousand Unit Level

The second key demand is for enterprises to proactively pursue an “internal closed loop.” Unlike the traditional approach focused on low-cost manufacturing, modern mobile robotics companies prefer to highly integrate critical functions—including headquarters operations, R&D, manufacturing, testing, and application—within a single facility. For example, EULAI plans to establish its headquarters as a modern industrial base that integrates R&D, manufacturing, testing, and corporate management, clearly reflecting the company’s strategic commitment to integrating key functions. Such an internal closed loop also enables more agile responses to evolving market demands.

Furthermore, the growing demand within specific market segments has driven companies’ current factory expansions and production increases, particularly in the heavy-duty mobile robotics sector. EULAI invested RMB 1.1 billion to establish its R&D headquarters, aiming for an annual production capacity of 600 heavy-duty robots; meanwhile, MORTISEON partnered with Haipeng Group to launch a project with an annual output of 500 units. The concentrated implementation of these large-scale projects—each producing hundreds of units—clearly demonstrates the robust application market demand in this sector.

External policy guidance and financial support have played a crucial role in driving this wave of production expansion. Competition among local governments in the robotics industry has intensified, with proactive measures such as prioritizing industrial land allocation, investing through local industrial funds, and providing park-related subsidies to attract robotics companies to establish production bases locally.

The most strategically profound requirement lies in strengthening cluster-based industrial thinking, where enterprise site selection places greater emphasis on synergistic collaboration with upstream and downstream ecosystem partners. The close physical integration among upstream and downstream enterprises enables a fully closed-loop process spanning sensor supply, algorithm debugging, system integration, and scenario testing. At this stage, factory construction is no longer an isolated asset investment but rather a strategic initiative through which enterprises connect with supply chain partners to build a highly collaborative value community.

In summary, from the fundamental requirement for market survival, to the cornerstone of capability encompassing large-scale production capacity and a closed technological loop, to the developmental imperative of expanding into specialized segments—with policy support—these five driving forces progressively converge to chart an ecological path for industrial clusters, collectively propelling mobile robotics enterprises toward comprehensive transformation.

Conclusion

The wave of mobile robot factory deployments from 2025 to early 2026 has evolved into a comprehensive restructuring of the entire industrial chain, centered on manufacturing capabilities.

Of course, behind the prosperity lies room for sober reflection. A significant number of factories exhibit a notable time lag between their designed production capacity and the currently validated market absorption capacity; when integrated R&D and manufacturing becomes a hallmark of enterprises, their competitive differentiation will be truly solidified through technological depth and ecosystem cohesion.

From May 21 to 22, 2026, the Second Global Unmanned Forklift Application Scenario Competition & the Material Handling and Sorting Challenge for Embodied Wheeled Humanoid Robots 2026 will be held in Hangzhou by China Mobile Robot Industry Alliance (CMRA) and Humanoid Robot Scene Application Alliance (HRAA) Building upon the existing unmanned forklift category, this event introduces a dedicated wheeled humanoid robot track for the first time, addressing the industry’s practical needs for embodied intelligence applications and further bridging technological innovation with industrial implementation.