In the first half of 2026, Skild AI—an artificial intelligence unicorn—completed a transaction that struck the mobile robotics industry as highly unconventional: it acquired the robotics automation business of Zebra Technologies. Zebra is a renowned player in the global warehousing IoT sector; after years of strategic positioning, it announced plans to scale back and divest its robotics business in late 2025. The ultimate buyer was not another robotics company, but rather an AI enterprise whose core competitiveness lies in foundational models.

This transaction, characterized by an unexpected shift in roles, serves as a key clue to understanding the wave of M&A activity in the mobile robotics sector during the first half of 2026. The industry has moved beyond the phases of simple capacity expansion and “land-grabbing” market share battles, entering a critical juncture defined by the reshuffling of existing market players and a qualitative leap in technology. Industry capital and leading players alike have realized that the growth dividends from single-technology approaches are drying up; the only path to a breakthrough lies in horizontal and vertical supply chain integration and the construction of a comprehensive ecosystem.

This round of industry consolidation is not merely blind capital expansion; it is an evolutionary process focused on filling product gaps, betting on embodied AI, accelerating AI deployment, and breaking down the boundaries between application scenarios.

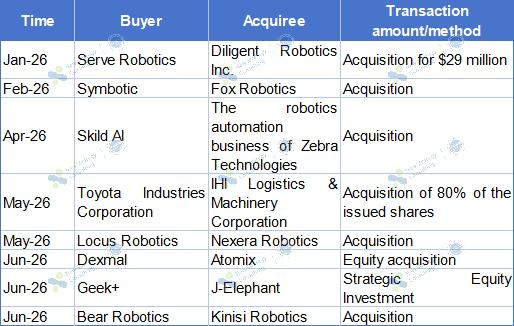

(Based on incomplete statistics compiled by the New Strategy Mobile Robot Industry Research Institute (NSRI) from public data as of June 23.)

Buy What They Lack: Horizontal Category Expansion and Vertical Scenario Extension

The warehousing and logistics robotics sector is undergoing a profound restructuring characterized by the horizontal expansion and vertical extension of product lines. After years of development, commoditization and fierce competition within traditional market segments have become increasingly apparent. Leading enterprises are no longer attempting to build complete product portfolios from scratch; instead, they are using capital operations to precisely “fill in the puzzle pieces” around their existing strengths.

A distinct trend observed in the M&A deals of the first half of the year is that mobile robotics companies are prioritizing acquisitions to plug gaps in their product matrices or to leverage the customer bases and application experience of target companies—thereby creating more opportunities to validate their existing products in real-world settings—rather than rashly entering entirely unfamiliar business domains. This underlying logic of “buying what is missing” is rapidly evolving along two main tracks: horizontal product category expansion and vertical application scenario extension.

This image is generated by AI.

Regarding horizontal product category expansion, the core objective for enterprises is to acquire key technologies or diversify product offerings through mergers and acquisitions, thereby rapidly building more comprehensive, full-scenario solutions.

A clear example of acquiring key technology is the acquisition of the Canadian robotic grasping technology company Nexera Robotics by Locus Robotics, a leading player in the global warehouse Autonomous Mobile Robot sector. While Locus Robotics has long excelled in warehouse logistics with AMRs known for stable navigation and efficient in-warehouse collaboration, its products have consistently faced a critical limitation: insufficient grasping capabilities. The acquisition has a clear, focused objective: to deeply integrate Nexera’s NeuraGrasp™ technology into the next-generation Locus Array platform, thereby comprehensively enhancing mobile manipulation capabilities. Crucially, Nexera’s core technical team will join Locus Robotics, and their solutions will be rolled out in customer projects over the coming months, enabling Locus Robotics to transition from “robot-assisted picking” to “autonomous robotic picking.”

A similar logic of capability enhancement is evident in Bear Robotics’ acquisition of Kinisi Robotics. Although Bear Robotics has deployed over 16,000 commercial robots and established a global commercial network, its robots have historically been limited to navigation and delivery, lacking object manipulation capabilities. In contrast, Kinisi Robotics specializes in wheeled humanoid robots; its core technology focuses on robot manipulation, Vision-Language-Action (VLA) models, and foundational robotics models, providing key capabilities such as grasping, transport, and sorting. Following the acquisition, Bear Robotics can layer advanced task capabilities onto its existing platform, potentially expanding the operational scope of its robots to achieve full-scenario automation covering transport, cleaning, picking, and sorting.

Additionally, Geek+, a leading warehouse robotics company, has chosen a “lighter” investment path to enrich its product portfolio. Geek+ has a deep presence in smart logistics, boasting a mature global network, integrated scheduling capabilities, and extensive experience in large-scale deployments. Meanwhile, J-Elephant possesses differentiated expertise in pallet-based automated storage and retrieval systems (AS/RS) and lightweight robotic solutions, creating a perfect complementary fit. By entering the market through investment rather than M&A, Geek+ has rapidly expanded its product line while maintaining the flexibility of its partnerships. For the high-density automated storage sector—a field still undergoing technological evolution—this is a pragmatic integration approach that aligns with the company’s “open and win-win” ecosystem strategy.

Unlike the previous two examples, which focused on technology and product modules, the acquisition of autonomous forklift manufacturer Fox Robotics by the US warehouse robotics firm Symbotic achieved both product supplementation and channel synergy—a “product-plus-channel” reinforcement. Symbotic’s revenue relies heavily on Walmart, and Fox Robotics also supplies Walmart; thus, this acquisition not only filled a gap in the forklift product line but also effectively integrated a supplier already trusted by a key client directly into its own system. More importantly, forklifts—as standardized equipment that is flexible to deploy and has a relatively low barrier to entry—serve as a “foot in the door” for Symbotic to establish relationships with a broader range of warehouse clients. This move simultaneously enriched the product portfolio and expanded deployment scenarios by leveraging Fox Robotics’ existing customer relationships, representing a simultaneous push for horizontal product expansion and vertical channel deepening.

Turning to “vertical application scenario expansion,” the driving force behind M&A in this category is not a lack of products, but rather the absence of an “entry ticket” or engineering delivery experience required to access specific, high-barrier scenarios. In such transactions, the buyer already possesses a comprehensive product matrix but is constrained by barriers specific to certain industries or physical environments.

Toyota Industries Corporation’s acquisition of an 80% stake in IHI Logistics & Machinery Corporation is a classic example of a traditional forklift giant strengthening its engineering delivery capabilities for vertical scenarios. While Toyota Industries already possessed robust R&D capabilities for AGVs, forklifts, and warehouse control systems—along with a well-rounded product portfolio—its engineering delivery experience in food logistics and cold-chain logistics was relatively limited. Conversely, IHI Logistics & Machinery had long specialized in cold-chain logistics equipment and system integration. The two companies’ capabilities in this niche sector were highly complementary; what Toyota sought was not a brand-new product line, but rather an “entry ticket” and practical deployment experience for these specific, high-barrier scenarios. According to public information, the equity transfer is expected to conclude in April 2027, with full ownership achieved within five years; this phased approach reflects the strategic prudence of Toyota’s orderly integration within the logistics automation sector.

Meanwhile, the acquisition of Diligent Robotics by Serve Robotics—a U.S. developer of autonomous delivery robots—marks a strategic expansion across the boundary from outdoor to indoor operational environments. Serve Robotics originated in outdoor sidewalk last-mile delivery, with operations historically confined to outdoor settings, whereas Diligent Robotics focuses on indoor service and healthcare applications, possessing proprietary expertise in mobile manipulation. Upon completion of the acquisition, Serve will enter the indoor market for the first time, simultaneously establishing a presence in indoor services, mobile manipulation, and healthcare. It is reported that Serve Robotics will pay up to an additional $5.3 million contingent upon meeting specific milestones; the inclusion of such earn-out clauses reflects the buyer’s cautious expectations regarding the integration of these new operational scenarios.

While the paths taken in these transactions differ, the underlying logic remains consistent. The buyers have already established firm footholds in their respective niches; their M&A or investment activities represent precise strategic complements to existing strengths rather than attempts to start from scratch. Their decision to “buy” rather than “build” stems from a clear-eyed assessment of the time gap between R&D cycles and market windows—in an era of accelerating competition within the mobile robotics sector, there is simply no time to wait. Only by rapidly assembling a comprehensive capability portfolio through capital-driven moves can they secure a ticket to the next stage of competition before the window of opportunity closes.

AI Companies Enter the Robotics Market: Software-Driven “Hardware Augmentation”

Another noteworthy trend in this year’s M&A landscape is the move by AI companies to acquire robotics hardware businesses. This form of “reverse integration”—while historically rare in the mobile robotics M&A sector—has appeared frequently during the first half of 2026.

The acquisition of Zebra Technologies’ robotics automation business by the emerging AI unicorn Skild AI serves as a prime example of this trend. Zebra Technologies had announced plans in late 2025 to scale back and seek a strategic divestiture of its AMR business. This move represented a classic strategic retreat from the robotics sector by a traditional tech giant, driven by challenges such as high integration complexity, unclear paths to scalability, and limited synergy with its core business operations. Skild AI, the company taking over the business, is an AI unicorn whose core competitiveness lies in general-purpose foundation models for robotics. A key challenge in its technical approach is the need for real-world hardware environments to iterate and deploy its models; relying solely on software capabilities makes it difficult to establish a complete operational loop in the robotics sector. Acquiring Zebra Technologies’ AMR business provides Skild AI with a ready-made hardware platform, deployment case studies, and a customer network, transforming AI-driven robotics from a laboratory concept into a deliverable product ecosystem.

A similar dynamic is playing out in China. Domestic companies Dexmal and Atomix have pursued a comparable path, albeit from different starting points. Dexmal’s core asset is its general-purpose embodied AI foundation model, “DM0.” This model achieves cross-domain data integration and can execute general manipulation tasks across diverse hardware platforms—theoretically possessing the ability to operate independently of specific hardware configurations. Yet, this very strength presents a challenge: foundation models require continuous feedback from real-world physical systems to iterate effectively. Atomix’s hardware expertise and deployment experience in the logistics robotics sector perfectly bridge this gap. Their merger targets the large-scale deployment of embodied AI and global expansion, driven by the fundamental logic that foundation model evolution relies on interaction with the physical world, making an autonomous, controllable hardware platform a critical component.

The acquisitions involving Skild AI and Dexmal reflect a shared underlying logic: AI software companies are using M&A to directly incorporate robotics hardware assets. This represents the capitalization of the “software-defined, AI-driven” trend. When AI companies determine that developing hardware in-house takes too long and that ecosystem partnerships offer insufficient control, acquiring an existing hardware platform and deployment network becomes the most direct solution. Underlying this choice is a strategic assessment: the ultimate competitiveness of robotics products will increasingly hinge on software and AI capabilities rather than being anchored to the hardware itself.

If this logic holds, the competitive landscape of the mobile robotics sector will undergo profound changes. Previously, mobile robotics companies primarily competed against one another; in the future, however, AI companies armed with foundation models may enter the arena as integrators, reshaping the industry’s balance of power.

Eve of a New Era: Dissolution and Rebirth

Viewed from a broader perspective, the wave of M&A activity in the first half of 2026 transcends the strategic intentions of individual enterprises. When the collective pursuit of system integrity shifts from isolated strategic choices to a common industry trend, it signals a transition from point-based competition to a contest of system-level platforms.

First, this signifies a fundamental shift in the dimension of competition. Previously, companies in the mobile robotics sector typically established differentiated advantages based on one or a few technical dimensions. However, the consolidation seen in the first half of the year demonstrates that leadership in a single dimension is no longer sufficient to create a long-term competitive moat. Whether it is the merger of Dexmal and Atomix via equity acquisition, or Skild AI’s incorporation of Zebra Technologies’ AMR business, the ultimate objective is the same: to control the three critical links of “data entry points, algorithmic iteration, and hardware deployment.” The players who remain in the game will be system-level platforms capable of integrating the entire value chain, rather than technical champions in a single segment.

Second, the industry’s value center is shifting significantly from hardware to data and algorithms. The underlying logic behind the AI companies acquiring hardware assets in the aforementioned deals goes beyond merely “filling out product lines”; it is about securing real-world physical interaction data and an environment for continuous model iteration. This implies that real-world scenario data—generated through large-scale deployments—will become a core asset for robotics enterprises. The company that operates the most robots and covers the widest range of physical environments will enable its AI models to evolve faster, thereby creating a virtuous “flywheel” effect. This revaluation of value will profoundly influence corporate valuation logic and capital allocation strategies.

Even more far-reaching is the accelerating dissolution of industry boundaries. The mobile robotics and artificial intelligence sectors are deeply converging; while the rules of competition have not yet fully crystallized, the contours of a new industrial landscape are already emerging. “Composite players”—those possessing in-house general-purpose AI models, hardware deployment capabilities, and scenario-based deployment networks—are poised to take the stage. This shift will compel the supply chain structure to move from “vertical division of labor” to “horizontal integration,” shift talent requirements from “single-discipline engineering backgrounds” to “AI + robotics + scenario” multidisciplinary expertise, and trigger a comprehensive re-evaluation of the industry’s capital valuation framework.

For companies still sitting on the sidelines, the window of opportunity to rely on independent, single-point capabilities is rapidly closing. Traditional industry boundaries are dissolving at an accelerating pace, and while growing pains are inevitable, a new era of mobile robotics—smarter, more flexible, and truly ubiquitous—is clearly visible on the horizon. For every participant, this is not merely a contest of technology or capital, but a pivotal struggle to redefine the future of robotics.