According to Low-speed Automated Driving Industry Alliance (LSAD), on May 29, MINIEYE announced the acquisition of a 50% stake in Xi’an Tongtu Technology Co., Ltd., a wholly-owned subsidiary of ZTO Express, a leading domestic integrated logistics company, for a total consideration of RMB 25 million. Upon completion of the acquisition, Tongtu Technology will become a non-wholly-owned subsidiary of MINIEYE.

Through the acquisition, MINIEYE will integrate Xi’an Tongtu Technology’s smart logistics operation scenarios and resources, combined with its own autonomous driving technology, to accelerate the commercialization of L4 unmanned vehicles in the logistics field and strengthen its market competitiveness in the smart logistics sector.

It is worth noting that, according to incomplete statistics from LSAD, since 2026, the global autonomous driving industry has seen more than 10 M&A and consolidation cases, covering vehicle manufacturers, parts suppliers, and end-user companies, indicating a comprehensive and accelerating wave of industry consolidation.

Who buys? Who sells?

The intelligent driving chip and perception fields have fired the first shot.

On January 2, 2026, Black Sesame Technologies strategically acquired EEASY TECH, strengthening its technological and product advantages in low-power, high-performance AI SoC chips and further extending its overall layout towards automotive-grade computing and edge intelligent solutions.

Following this, on January 6, Mobileye, Intel’s autonomous driving chip company, announced the acquisition of Israeli humanoid robot company Mentee Robotics for approximately $900 million. This acquisition aims to enhance the generalization capabilities of autonomous driving systems in complex scenarios and lay the groundwork for future applications of humanoid robots in logistics, services, and other scenarios.

Notably, before the buzz surrounding this acquisition had subsided, on April 15, news broke that Mobileye was also considering selling its mobility data platform, Moovit. This back-and-forth makes the ambitions of this autonomous driving chip giant even more unpredictable.

The automotive industry, especially unmanned delivery companies, is also expanding horizontally.

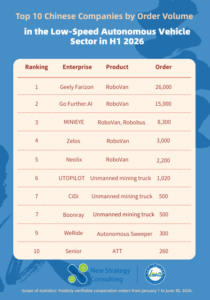

On January 20, US-based delivery robot company Serve Robotics announced its acquisition of Diligent Robotics, another company specializing in hospital delivery, for $29 million. On January 29, Zelos, a leading Chinese company completed a deep restructuring with Cainiao, and subsequently, at the end of March, invested nearly 1.2 billion yuan to acquire a 27% stake in A-share listed company RASTAR. In February, Tencent’s Guangxi Tencent Venture Capital strategically invested in NEOLIX, completing its ecosystem in AI big data models, computing power, and data, securing a foothold for the application of autonomous driving scenarios.

Including MINIEYE’s acquisition of a 50% stake in Xi’an Tongtu Technology, these series of acquisitions and consolidations in the unmanned delivery sector indicate that this segment, which entered the stage of large-scale production relatively early, is also experiencing a faster period of industry reshuffling.

Beyond the bustling unmanned delivery market, upstream software companies, component manufacturers, and downstream scenario providers and terminal players are gradually converging towards the central region.

In April 2026, Atmos officially acquired Pronto AI, a leading company in autonomous driving for mining, accelerating the development of its “physical AI” concept. That same month, Caterpillar, a construction giant, acquired Monarch, an autonomous agricultural tractor startup, entering the unmanned agriculture field. At the end of May, Elbit Systems,,Israeli defense giant,, through its FUSE division, acquired Blue White Robotics, an autonomous driving kit company. This deal aimed to convert ordinary off-road vehicles into autonomous military and safety equipment and integrate them into its product line.

From “Single-Point Complementarity” to “Ecosystem Stitching”

Looking at the above series of acquisitions and integrations, it’s less a typical wave of industry mergers and acquisitions and more a belated movement of “ecosystem stitching.”

Previously, there were clear boundaries between participants in the autonomous driving industry, and many acquisitions revolved around vertical sectors. However, LSAD observes that this series of mergers and acquisitions in the first half of 2026 is further dismantling the barriers between technology, scenarios, and data, presenting a new logic.

First, there’s the resource exchange driven by the “scenario-centric” approach.

Whether it’s Cainiao injecting its autonomous vehicle business into Zelos, or MINIEYE acquiring Xi’an Tongtu under ZTO Express, the core logic is no longer simply technology acquisition, but a deep integration of “technology provider + scenario provider.” This further illustrates that in the second half of the industry’s development, possessing real-world paid scenarios is a more valuable asset than mere technological prowess.

Second, there’s the cross-industry spillover of “generalization capabilities.”

Mobileye’s acquisition of Mentee Robotics, Atmos’ integration of Pronto AI, and Caterpillar’s acquisition of Monarch—these transactions demonstrate that perception and decision-making capabilities validated in numerous autonomous driving scenarios are being generalized back to the entire autonomous vehicle. Whether these companies can successfully realize their “generalization capabilities” is a key focus for the industry.

Finally, there’s the strategic focus of “weighting and slimming down.”

For example, Mobileye is simultaneously investing heavily in robotics while rumored to be selling its Moovit mobility data platform. This shift—from advancing to retreating—represents leading companies divesting non-core businesses and concentrating their efforts on commercialization, a prominent trend in the overall wave of mergers and acquisitions.

In summary, ecosystem co-construction capabilities are becoming crucial for breaking through the challenges in the second half of the autonomous driving industry. Against this backdrop, how to address the pain points of low-speed autonomous driving in scenarios such as logistics, mining, and ports, and explore new paths for deep integration of technology, capital, and application scenarios, will be key issues of focus for the industry going forward.

From July 9 to 10, 2026, the 6th Low-Speed Autonomous Driving Scenario Ecosystem Collaboration and Expansion Conference 2026 will be held. Industry stakeholders from across the supply chain will gather to engage in in-depth discussions on topics such as large-scale operations, ecosystem synergy, and cost reduction and efficiency improvement. Concurrent events include the Intelligent Sanitation: Technology Evaluation and Accreditation Competition of Municipal Cleaning Robots 2026, the 6th Low-Speed Autonomous Driving Industry G30 Summit 2026, and the 3rd High-Quality Low-Speed Autonomous Driving Supply Chain Exhibition (LSDS).

This is not merely a conference for analyzing industry trends, but also a practical platform for product testing, partner exploration, and collaborative development of a closed business ecosystem. In July, let us gather in Jinhua to witness how low-speed autonomous vehicles evolve from isolated advancements to coordinated fleet operations, collectively mapping out a trillion-dollar blueprint for low-speed autonomous driving.