Money is rapidly flowing into the embodied AI sector. With each round of financing and valuation increase, a batch of embodied AI robot unicorns worth tens of billions of yuan are emerging.

In this process, a noteworthy new phenomenon is emerging: some leading companies are no longer content with simply being “invested companies,” but are actively becoming industry investors, even personally incubating upstream and downstream projects.

In April 2026, several leading embodied robot companies appeared in the financing cases of Delta Intelligence and ARCHEBASE. Delta Intelligence completed an angel round of financing of over 100 million yuan, with investors including Leju Robot, AGIBOT, and Galaxea AI; ARCHEBASE completed an angel round of financing of tens of millions of yuan, with investors including PsiBot, NOEMATRIX, Zhejiang Humanoid Robot, and AI2 Robotics.

This indicates that the embodied AI industry is moving from product competition between individual companies to systemic competition in ecosystems, supply chains, data, and technological capabilities.

Among them, AGIBOT, Leju Robot, GALBOT, and Galaxea AI are representative companies with relatively more external investment activities.

- AGIBOT: From the Robotics Manufacturertothe Industry Chain Investment Platform

The most representative example is AGIBOT. Over the past two years, it has rapidly advanced its product, technology, and commercialization layout while continuously expanding its industrial footprint through joint ventures, incubation, and direct investment.

Public information shows that AGIBOT has not only established joint ventures with several listed companies but has also internally incubated several subsidiaries focusing on key links in the robotics industry chain. For example, BOTSHARE focuses on robot leasing, AGILINK enters the dexterous hand market, Maniformer focuses on embodied data, and AGIQUAD focuses on quadruped robots. This internal incubation reflects AGIBOT’s segmented layout around the key links of “robots from R&D to deployment.”

More noteworthy is that AGIBOT is also accelerating its platformization at the capital level. According to business registration information, as of May 2026, AGIBOT had invested in 21 projects across the robotics industry chain, covering multiple areas including robot bodies, embodied intelligent brains, force control, haptic feedback, computing platforms, core components, application solutions, and health companionship.

From the perspective of investment projects, AGIBOT’s layout can be roughly divided into four categories.

The first category is robot body and complete machine manufacturers. These include companies such as AheadForm, Spatialtemporal AI, Smart Multiplication Robotics, GENISOM AI, AiMOGA, XDream Robotics, Yushu Intelligent, SIR Robot, and DIGIT.

The second category is embodied intelligent brains and AI platforms. These include companies such as Delta Intelligence, PsiBot, Huixi Intelligent, and XYZ Embodied AI. Among them, Delta Intelligence and PsiBot focus on embodied AI R&D, Huixi Intelligent is positioned as an embodied AI computing platform supplier, and XYZ Embodied AI focuses on general-purpose embodied brain R&D.

The third category is core components and perception and control capabilities. These include companies such as LinkTouch, LINKHOU, Xense Robotics, and FULLING Motor. LinkTouch focuses on cutting-edge force control technology for robots, LINKHOU enters the field of intelligent manufacturing and embodied AI core components, Xense Robotics focuses on multimodal tactile perception, and FULLING Motor provides control motors and system integration solutions.

The fourth category is application and solution projects. These include Flycode, ISHO, Fullive.AI, and Huazhi Tiancheng. Flycode focuses on robot application solution integration, Jinri Yixiu and Fullive.AI are related to health and living spaces, and Huazhi Tiancheng is in the direction of industrial internet technology development. While these projects are not entirely limited to the robot itself, they help AGIBOT understand end-user application scenarios and the needs of industrial customers.

Therefore, AGIBOT’s investment portfolio is not simply financial investment, but more like a “supply chain puzzle” built around its core business. The goal is to incorporate as many key capabilities as possible—from technology research and development to large-scale deployment—of embodied intelligent robots into its own ecosystem network.

- Leju Robot: Filling the Gaps Between Dexterous Hands and Embodied Intelligent Bodies

Leju Robot is also one of the more active investors in the embodied AI industry recently.

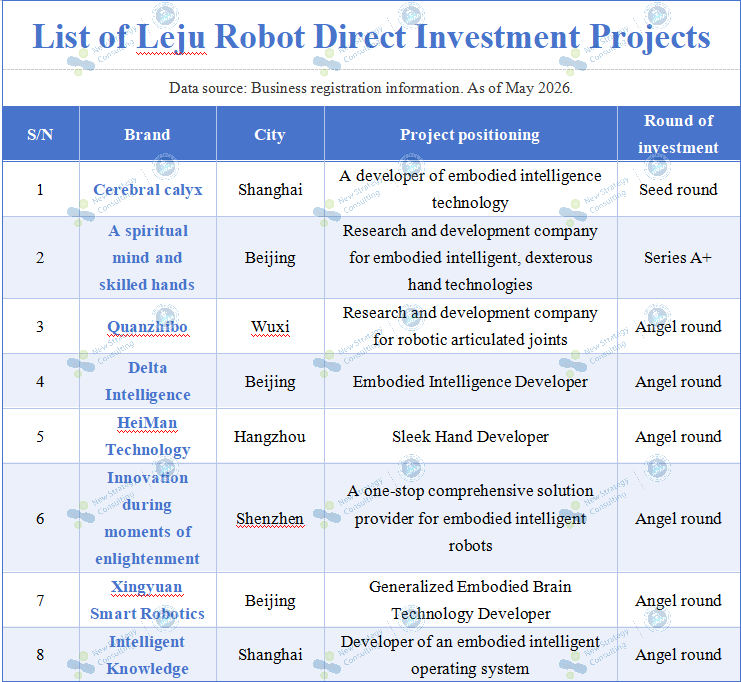

According to business registration information, as of May 2026, Leju Robot had invested in eight related projects, including EBKernel, LINKERBOT, Motorevo Robotics, Delta Intelligence, Heyman Tech, Woosh, XYZ Embodied AI, and Jushi Intelligent, covering areas such as embodied AI, dexterous hands, joint modules, embodied brains, and one-stop integrated solutions.

From its investment portfolio, Leju Robot’ strategy exhibits a strong “technology complementarity” characteristic.

On one hand, it has invested in companies related to dexterous hands, such as LINKERBOT and Heyman Tech. On the other hand, Leju is also focusing on the “brain” and core control capabilities of embodied AI. For example, Delta Intelligence positions itself as an embodied AI developer, XYZ Embodied AI focuses on the development of general-purpose embodied brain technology, and Motorevo Robotics is a developer of integrated robot joints.

Furthermore, Woosh positions itself as a one-stop integrated solution provider for embodied intelligent robots, and Jushi Intelligent focuses on the development of embodied intelligent operating systems. These projects are closer to the robot platform and application layers, helping Leju form a more complete ecosystem support for subsequent application scenarios.

Overall, Leju Robot’ investment scale is not as extensive as AGIBOT, but its focus is relatively concentrated: extending from the humanoid robot’s physical capabilities to dexterous hands, joints, embodied brains, operating systems, and solutions. Its investment logic leans more towards “physical capability enhancement,” that is, strengthening the robot’s comprehensive capabilities from movement to operation, and from hardware to intelligence by investing in key technology segments.

- GALBOT: Focusing on Cutting-Edge Technologies and Early Positioning

Compared to AGIBOT, GALBOT has fewer external investments, but its direction is also clear.

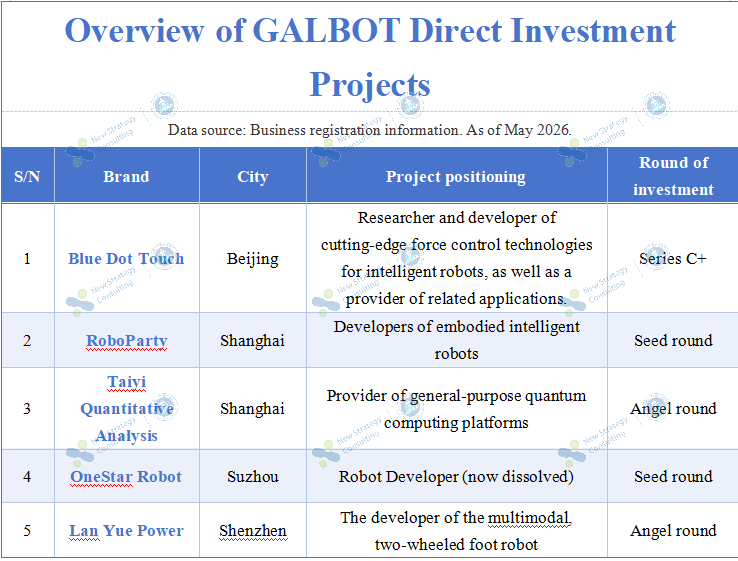

According to business registration information, as of May 2026, GALBOT’s direct investments included LinkTouch, RoboParty, Taiyi Liangsheng, OneStar, and Moon Dynamics, totaling 5 projects.

From the perspective of project positioning, GALBOT’s investments are more focused on cutting-edge technologies and robot hardware. LinkTouch focuses on cutting-edge force control technology for robots, RoboParty is positioned as a developer of embodied intelligent robots, Taiyi Liangsheng is a supplier of general-purpose quantum computing platforms, OneStar is a robot developer, and Moon Dynamics focuses on multimodal bipedal robots. This approach differs significantly from the broad-coverage industry chain strategy of AGIBOT. GALBOT has not made large-scale investments in traditional robot chains such as motors, supply chains, and application scenarios. Instead, it focuses on early positioning around future intelligent capabilities, new robot forms, and underlying technologies.

This is closely related to GALBOT’s own positioning. As a company with general-purpose robots and embodied AI as its core focus, GALBOT has long emphasized the generalization capabilities of robots, their adaptability to complex scenarios, and the exploration of future intelligent forms. Therefore, its investment portfolio revolves more around the “next-generation robot capability boundaries.”

- Galaxea AI: Building an Ecosystem Around the Embodied AIBrain

Galaxea AI’s investment portfolio also exhibits distinct characteristics.

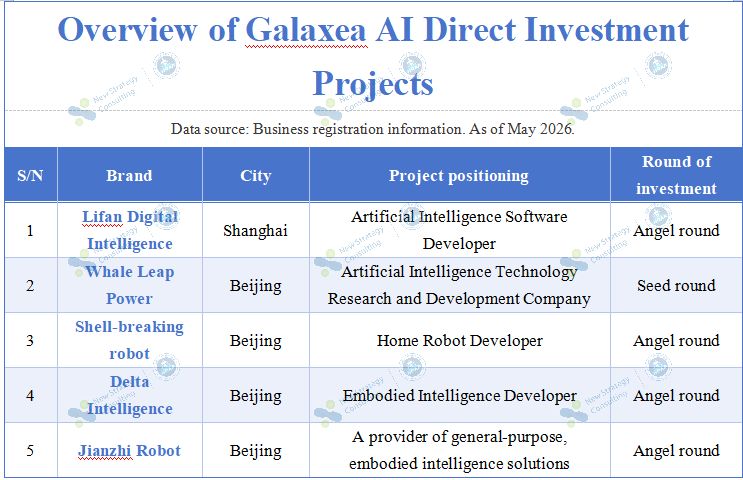

According to business registration information, as of May 2026, Galaxea AI’s direct investments included five companies: Liulan Digital Intelligence, Whale Leap, PokeBot, Delta Intelligence, and GenRobot.AI.

From a project positioning perspective, Galaxea AI leans more towards AI software, artificial intelligence research, embodied AI, and general embodied AI solutions. Liulan Digital Intelligence positions itself as an AI software developer, Whale Leap as an AI technology R&D company, Delta Intelligence focuses on embodied AI, GenRobot.AI is a general embodied AI solution provider, and PokeBot targets home robot R&D.

It’s worth noting that Huazhe Xu, the founder of PokeBot, is the former co-founder and chief scientist of Galaxea AI. This means that some of Galaxea AI’s investments are not merely simple financial investments, but also involve a certain degree of technical team extension and ecosystem incubation.

Overall, Galaxea AI has not made a large-scale entry into the traditional hardware supply chain like AGIBOT, nor has it focused on robot form innovation like Galbot. Instead, it focuses more on AI capabilities, the embodied AI “brain,” general solutions, and future home scene entry points.

- Why are leading companies starting to invest?

There are several reasons behind the leading embodied AI companies starting to invest externally.

First, embodied AI is a typical long-chain industry. For a robot product to truly become commercialized, it requires the collaboration of multiple links, including the robot body, joints, motors, reducers, sensors, dexterous hands, control systems, AI models, data acquisition, simulation training, scene deployment, and after-sales service. Relying solely on internal R&D is insufficient to cover all capabilities. Investment allows leading companies to quickly fill gaps in their capabilities.

Second, industry competition is shifting from single-point technology competition to ecosystem competition. Early-stage companies competed on whether robots could walk, run, and complete demonstration tasks. The next stage will focus on cost, mass production, data loops, scenario implementation, and continuous iteration capabilities. Investing in upstream and downstream projects is essentially building an ecosystem moat in advance.

Third, leading companies need to secure key resources. The embodied AI industry is still in its early stages, and the number of excellent teams in sensing, actuators, force control, data, and modeling is limited. Early-stage investment allows companies to establish deeper partnerships with potential key suppliers, technology partners, and ecosystem companies.

Fourth, the capitalization process is changing the role of companies. As the valuations of leading embodied AI companies rapidly increase, some companies have developed stronger financing and capital operation capabilities. They not only need to tell investors their growth stories but also begin to use capital to amplify their industry influence.

Fifth, investment is also a form of strategic trial and error. The future applications of embodied AI are not yet fully defined, but significant opportunities may emerge in areas such as industry, commerce, home, healthcare, education, and companionship. By investing in multiple projects with small stakes, leading companies can observe the real-world progress of different technological approaches and scenarios before deciding on their future investment priorities.

Conclusion: Represented by companies like AGIBOT, GALBOT, Galaxea AI, and Leju Robot, leading embodied AI companies are transitioning from “fundraisers” to “investors.” Their investment styles differ: AGIBOT leans towards broad industry chain coverage, GALBOT focuses on early-stage positioning in cutting-edge technologies, Galaxea AI emphasizes building an intelligent ecosystem, and Leju focuses on supplementing key capabilities around the humanoid robot itself.

The competition in embodied AI is evolving from “who makes the robot first” to “who can organize a more complete industrial system.” In the future, the companies that truly succeed may not only be the most technologically advanced but also the ones best able to integrate capital, supply chains, data, models, and scenario resources.

On June 25, the “3rd Embodied Humanoid Robot Scenario Application Expansion Conference 2026” will be held in Hangzhou, bringing together top industry experts, leading scenario providers, and benchmark companies to showcase the latest technologies and implementation cases. For registration, please click https://luma.com/qgx5g1em.