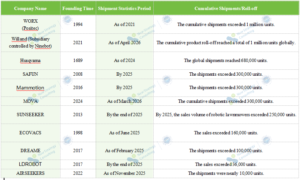

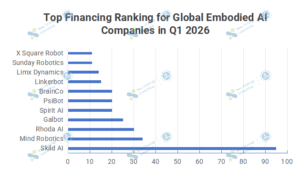

On July 14, 2026, LimX Dynamics announced the completion of a pre-IPO funding round raising nearly $200 million, bringing its post-money valuation to RMB 15 billion. This financing propelled LimX Dynamics into the ranks of “unicorn” companies valued at over RMB 10 billion and officially added it to the expanding cohort of embodied AI companies pursuing IPOs.

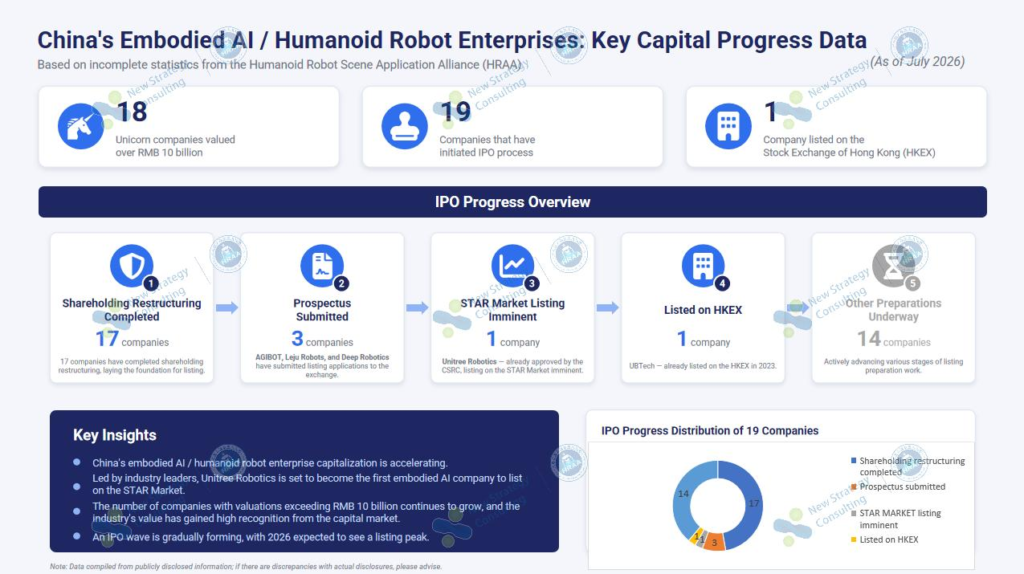

According to incomplete statistics from the Humanoid Robot Scene Application Alliance (HRAA), 18 Chinese companies focused on “embodied AI and humanoid robots” have achieved unicorn status (valuations exceeding RMB 10 billion), with six of them valued at over RMB 20 billion.

Meanwhile, the industry’s capitalization process is accelerating significantly. Currently, 19 embodied AI/humanoid robot companies have initiated the listing process; of these, 17 have completed joint-stock restructuring, three have submitted prospectuses, one is poised to list on the STAR Market, and one has already gone public.

Note: The scope of these statistics covers companies with “embodied AI and humanoid robots” as their core business; it excludes companies involved in broader categories of robotics, such as mobile robots, cobots, and service robots.

17 Companies Completed Restructuring and IPO Pipeline for Embodied AI Takes Shape

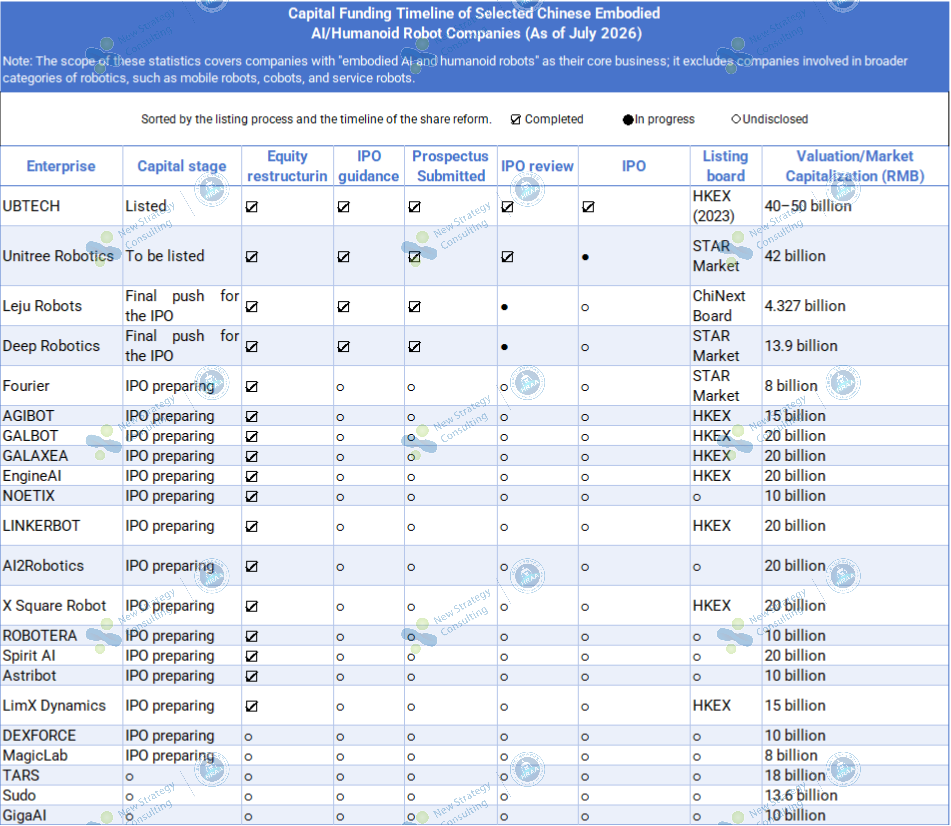

Among the 19 companies that have initiated the listing process, 17 have completed joint-stock restructuring. In addition to Unitree Robotics, Leju Robots, and Deep Robotics, this group includes Fourier Intelligence, AGIBOT, Galbot, GALAXEA, EngineAI, NOETIX, LINKERBOT, AI2Robotics, X Square Robot, ROBOTERA, Spirit AI, Astribot, and LimX Dynamics.

In terms of numbers, companies that have completed restructuring account for nearly 90% of the total number of companies that have started the listing process, which indicates that capitalization preparations in the embodied AI industry have evolved from the initiatives of a few leading players into a collective move by a broader group of companies.

Joint-stock restructuring is a crucial foundational step for companies entering the capital market. After converting from a limited liability company to a joint-stock company, the enterprise must further standardize its equity structure, corporate governance, financial management, related-party transactions, and employee shareholding arrangements, thereby paving the way for pre-listing guidance and subsequent IPO applications.

However, completing this restructuring merely establishes the foundation for advancing the listing process. The journey from shareholding restructuring and IPO guidance to the formal filing of a listing application involves business streamlining, financial standardization, and adjustments to shareholder structures. Although some enterprises have completed shareholding restructuring, they have not yet publicly disclosed their advisory agencies or target market boards; consequently, actual filing timelines vary significantly.

Currently, apart from UBTECH, which listed in 2023, only three enterprises have truly entered the public filing stage. Unitree Robotics and Deep Robotics have opted for the STAR Market, while Leju Robots has chosen the ChiNext board.

Among them, Unitree Robotics has made the most rapid progress. On July 1, 2026, the China Securities Regulatory Commission (CSRC) issued an approval for Unitree Robotics’ IPO registration, publicly disclosing the decision on July 2. Having completed the exchange review and CSRC registration, the company must still finalize the issuance, subscription, and listing of shares; thus, it is currently in a state where registration is complete, but the official listing has not yet occurred.

Leju Robots has submitted its prospectus to the ChiNext board, while Deep Robotics has submitted its prospectus to the STAR Market. The subsequent review processes for these two companies will provide further insight into the listing pathways available to different types of embodied AI enterprises in the A-share market.

Through Dual Tracks of A-Shares and Hong Kong Stocks, Industry Capitalization Enters the Realization Phase

Current progress indicates that Chinese embodied AI enterprises are establishing two primary listing pathways: the Hong Kong stock market and the A-share market.

The Hong Kong stock market is currently the preferred choice for leading embodied AI enterprises. UBTECH listed there in 2023, becoming the only company within the scope of this analysis to have successfully completed its listing. Meanwhile, companies such as Agibot, Galbot, GALAXEA, EngineAI, LINKERBOT, and X Square Robot are viewed by the market as potential candidates for future Hong Kong listings.

Compared to the A-share market, the Hong Kong market holds particular appeal for technology enterprises that are still in a phase of high R&D investment and possess relatively complex shareholder structures; it also offers greater flexibility for capital operations to companies that have not yet achieved stable profitability.

However, judging by public progress, most companies, with the exception of UBTECH, remain in the stages of shareholding restructuring or IPO preparation and have not yet formally submitted listing applications. Although the Hong Kong market attracts a higher concentration of leading enterprises, the number of companies that have actually entered the public filing stage remains limited.

In the A-share market, two distinct pathways have emerged: the STAR Market and the ChiNext board. Both Unitree Robotics and Deep Robotics have targeted the STAR Market for their listings. For robotics companies that emphasize core technologies, independent R&D capabilities, and a focus on technological innovation, the STAR Market aligns well with their business positioning.

Leju Robots, on the other hand, has opted for the ChiNext board. Compared to the STAR Market, ChiNext places greater emphasis on growth potential, innovation capabilities, and the level of industrial integration; it may be better suited for embodied AI companies that have already established product deployment capabilities and a revenue base.

The push by companies to accelerate their listings is closely linked to the overall rise in industry valuations. High valuations provide greater financial flexibility for companies to undergo shareholding restructuring, bring in strategic investors, and prepare for IPOs, while simultaneously increasing the pressure to deliver strong financial performance post-listing.

Once in the public market, companies must substantiate their valuations through revenue growth, product delivery, customer acquisition, and commercialization capabilities. The valuation logic established in the private market, often based on technological expectations and industry growth potential, will increasingly face the rigorous scrutiny of the public market.

Conclusion:

From the 17 companies that have completed shareholding restructuring and the three that have submitted prospectuses, to Unitree Robotics completing its registration and UBTECH listing on the HKEX, Chinese embodied AI companies have formed a comprehensive capital pipeline spanning from pre-listing preparations to public market entry.

In the coming years, as more companies enter the listing process, the industry is likely to see significant differentiation: companies possessing core technologies, scalable delivery capabilities, and industrial resources will leverage the capital market to further expand their advantages, while those lacking a clear commercial path may face financing pressures and market elimination.

From the expansion of valuations into the RMB tens of billions to the formation of an IPO pipeline, China’s embodied AI industry is transitioning from a “capital-driven phase” to an “industry competition phase.” This competition, centered on technology, capital, and commercialization capabilities, has only just begun.

1-300x168.png)