In the field of industrial automation, unmanned forklifts are not a “new concept.” While they have moved away from the spotlight of consumer robots and humanoid robots, they have been undergoing slower but more predictable technological iterations and commercial validation within the manufacturing and logistics systems.

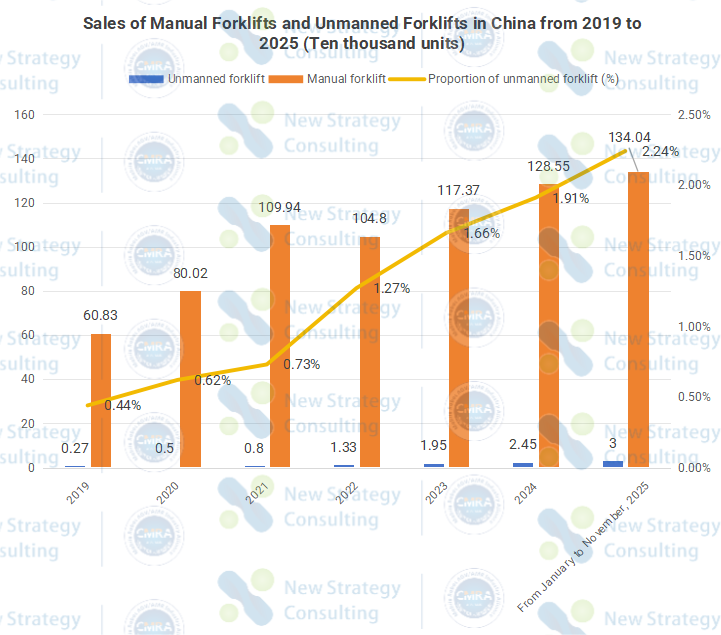

In 2025, the data provides the definitive answer. According to data from China Mobile Robot Industry Alliance (CMRA) and statistics from New Strategy Mobile Robot Industry Research Institute (NSRI), the sales of unmanned forklifts increased from 2,700 units in 2019 to approximately 24,500 units in 2024; our preliminary forecasts indicate that the sales may reach 30,000 units by 2025. This upward curve symbolizes the accelerated transition of unmanned forklifts from “niche pilot projects” to “large-scale applications.”

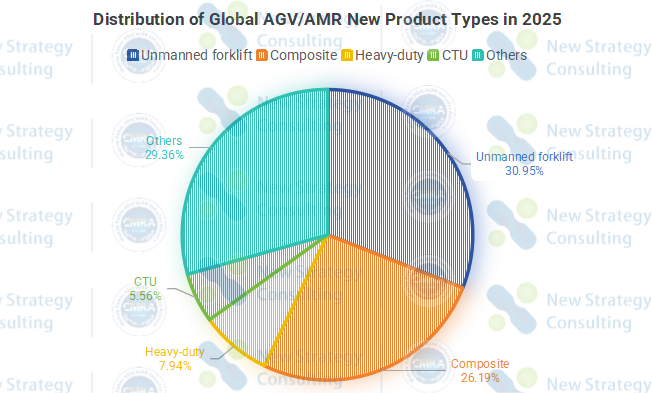

Market trends have directly ignited a race in R&D. Based on incomplete statistics from CMRA and NSRI, unmanned forklifts are one of the most promising categories within the mobile robot field. In 2025, a total of 126 new AGV/AMR products were released both domestically and internationally, including 39 unmanned forklifts, accounting for approximately 30.95%, maintaining its leading position among all product segments for several consecutive years. (Further reading: 126 New Mobile Robots Launched Globally in 2025)

Throughout the year, 32 companies released new unmanned forklift products. Chinese companies dominated in both quantity and pace, while German, Japanese, and American manufacturers maintained stable participation. This pattern reflects that unmanned forklifts have become fundamental equipment in the global industrial automation system, rather than a regional or phased product.

From a product structure perspective, unmanned forklifts are showing a clear trend of differentiation and refinement. Classified by forklift type, counterbalance forklifts, reach forklifts, pallet stacker forklifts, and pallet handling forklifts were all available in 2025. Classified by application scenario, products have gradually extended from standard warehousing to complex environments such as cold storage, narrow aisles, high-bay locations, and mixed indoor and outdoor operations.

The evolution of technological paths is the core factor supporting this change. Early unmanned forklifts primarily relied on laser reflector navigation. With the rapid development of intelligent driving technology, the capabilities of unmanned forklifts in path planning, dynamic obstacle avoidance, and multi-vehicle collaboration have significantly improved. Navigation methods have gradually shifted towards SLAM navigation, with laser SLAM currently being the mainstream choice in the market. Meanwhile, to meet the complex operational needs across indoor and outdoor scenarios, the application of advanced navigation solutions integrating multiple technologies is continuously expanding.

Looking at the 39 new products released in 2025, the application of SLAM navigation has become more widespread. Many new products are equipped with 3D SLAM, 3D laser SLAM, and other technologies, and most adopt integrated navigation modes such as laser + vision + GPS.

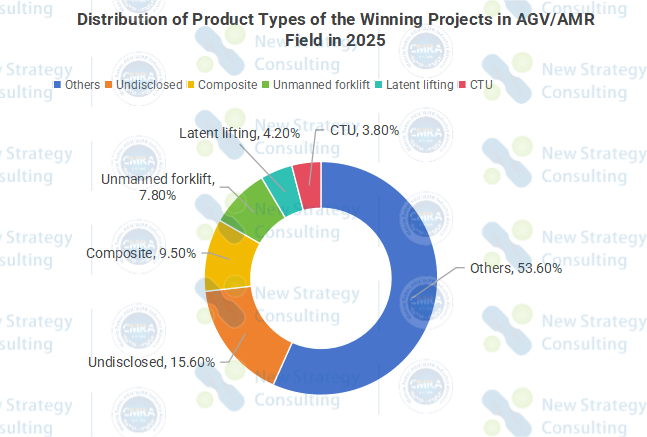

The depth of the market is often revealed in reality. The bidding data in 2025 serves as a mirror, reflecting the true aspirations of China’s manufacturing industry in the deep waters of transformation. According to data from CMRA and NSRI, among the 550 AGV/AMR projects disclosed in China throughout the year, unmanned forklifts firmly held a core position with 43 winning bids and a total disclosed value of approximately 412 million yuan.

From routine upgrades in smart warehousing parks to a super order from Moutai worth up to 200 million yuan, unmanned forklifts are becoming the most certain “lever” in the existing market competition, thanks to their highly mature business closed loop. In typical industrial scenarios such as heavy-duty, high-frequency, and continuous operation, unmanned forklifts, with their significant advantages in stability, operating efficiency, and total lifecycle cost, have become the irreplaceable priority option for enterprise automation transformation.

Meanwhile, the product types and technical routes of unmanned forklift winning bids in 2025 also showed more diverse characteristics, with different models and navigation solutions being repeatedly validated in the market. Behind this is a profound shift in user decision-making logic; the focus of users has shifted from “whether to adopt unmanned forklifts” to “whether they truly fit their production lines, warehouse structures, and process rhythms.” The increasing sophistication of market demands is further forcing industry manufacturers to upgrade from a single equipment supply model to a comprehensive capability integrating product, system, and scenario understanding.

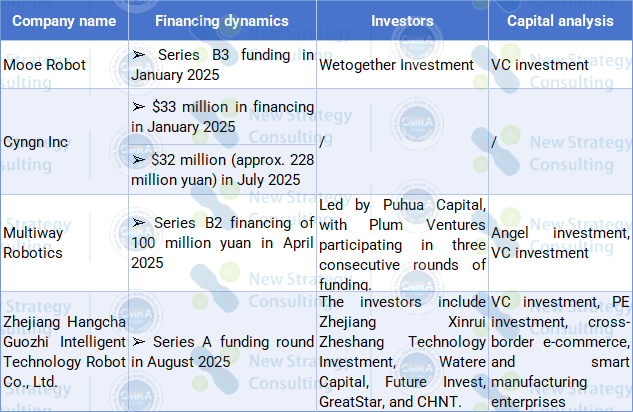

In 2025, despite a slight decrease in market enthusiasm, some unmanned forklift companies still attracted capital market attention, with financing rounds primarily concentrated in Series A and B stages. From the perspective of investors, VC and PE firms were the main players in this field, indicating a significant shift in capital evaluation criteria. Compared to the past, capital places greater emphasis on a company’s delivery capabilities, business model, and sustainable service capabilities, rather than simply betting on technological concepts or speculative trends. This change is gradually bringing competition in the unmanned forklift sector back to the fundamental logic of the industry.

In this fiercely competitive arena, there are traditional forklift companies, established AGV manufacturers, logistics integrators, and unmanned forklift manufacturers. The convergence of these four forces, while creating a fragmented competitive landscape, also fosters disruptive symbiotic possibilities.

As the industry matures, real-world capability validation is becoming increasingly crucial.

In May 2025, the world’s first unmanned forklift application competition was held by CMRA in Hefei. Leading global brands such as Heli, Linde, Hangcha Intelligent, EP, and NOBLELIFT competed on the same stage, undergoing systematic testing in a real industrial environment, providing the industry with a valuable comparative sample.

In 2026, CMRA will host the “Second Global Unmanned Forklift Application Scenario Competition & the Material Handling and Sorting Challenge for Embodied Wheeled Humanoid Robots 2026.” Building upon the unmanned forklift competition, a wheeled humanoid robot track will be introduced for the first time, responding to the industry’s real-world demand for humanoid robot applications and further building a bridge connecting technological innovation and industrial applications.

With the continuous opening of more real-world application scenarios, unmanned forklifts and related humanoid robot equipment are expected to unleash greater long-term value in the industrial logistics system.