At the beginning of 2026, embodied intelligence remains one of the most active sectors in the primary market.

According to statistics from China Humanoid Robot Scene Application Alliance (HRAA), as of February 25, there have been over 34 publicly disclosed funding events in this field this year, totaling nearly 20 billion yuan. A new round of funding news seems to be trending almost every few days.

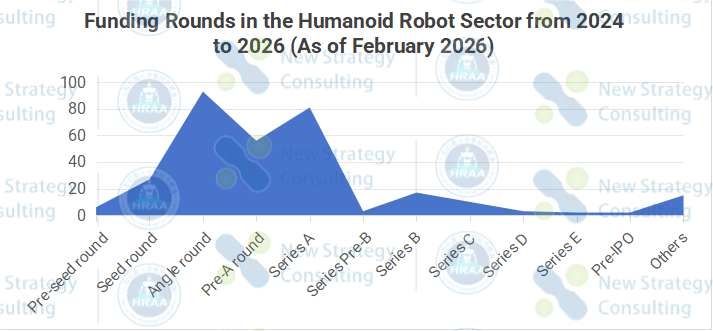

However, looking at a longer timeframe from 2024 to 2026, the situation presents a different picture: During these three years, there will be over 315 funding events related to embodied intelligence, of which only 34 are Series B or later. And only a dozen or so startups have actually completed Series B or higher funding.

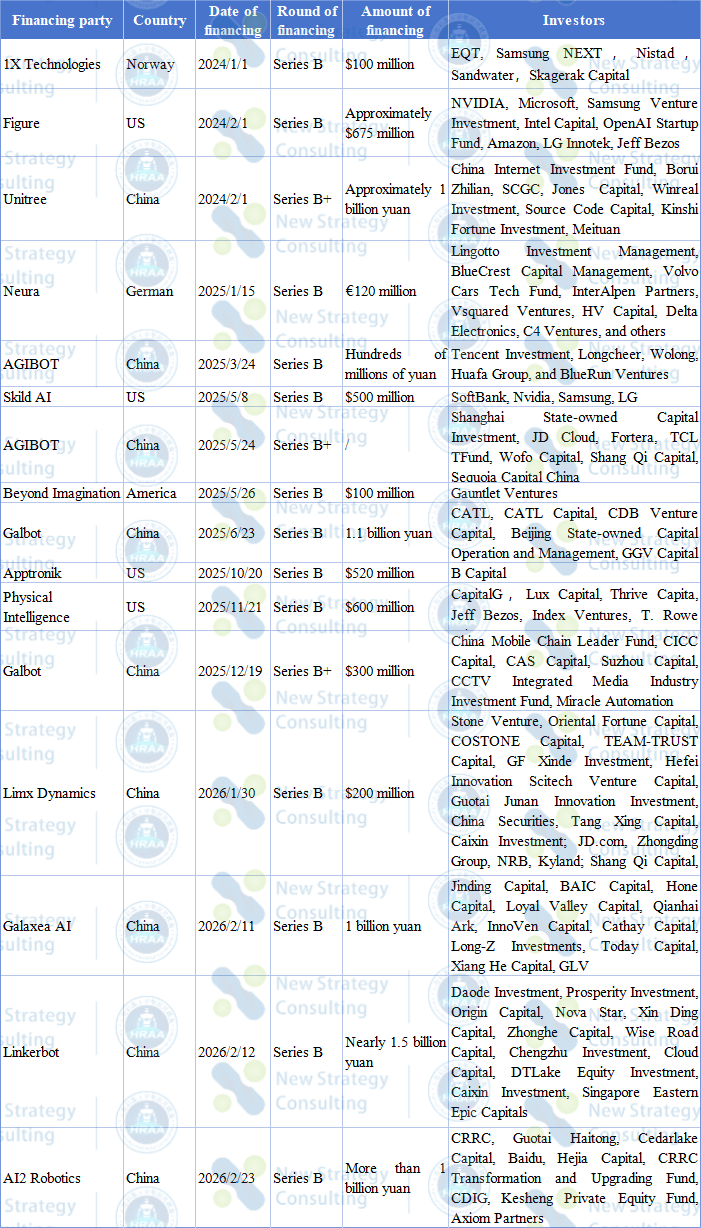

List of Series B Funding for Some Humanoid Robot Companies (Compiled from Publicly Available Online Information; in case of any inaccuracies, please make a correction.)

More importantly, in these 34 Series B and subsequent funding rounds, the vast majority of companies have raised over 1 billion yuan or even more in a single round. 1 billion yuan is becoming the “threshold” for embodied intelligence companies to cross the Series B funding threshold.

It is a common-sense story of how difficult it is to raise funds as you progress; but when the threshold is raised to 1 billion yuan, the gap no longer simply means “less money,” but rather a true industry watershed.

1. The Bustling Early-Stage Funding, and the Scarcity of Series B Funding

Let’s start with that most obvious dividing line.

Of the more than 300 funding events, most were concentrated in the seed, angel, Pre-A, and Series A stages.

A new track, a good story, and a technical team with star backgrounds and experience at large companies are often enough to secure seed funding. Venture capitals are willing to bet on “team + direction”: embodied intelligence under a large model sounds like the next-generation platform opportunity; it’s about choosing a side first.

But at Series B, the landscape changes drastically. Whether in China or overseas, very few companies can consistently advance past Series B.

More importantly, among those 30+ Series B and later funding rounds, the amounts show a very clear upward trend:

Norway’s 1X Technologies raised $100 million in early 2024; US-based Figure raised approximately $675 million in February of the same year; Skild AI, Apptronik, and Physical Intelligence all raised between $500 million and $600 million in their Series B rounds.

The same trend is observed in Chinese companies. After 2025, Galbot‘s Series B funding reached 1.1 billion yuan; Galaxea AI raised 1 billion yuan in early 2026; Linkerbot approached 1.5 billion yuan; AI2 Robotics disclosed “over 1 billion yuan”; and Limx Dynamics‘ Series B round was $200 million.

Over ten companies, more than ten Series B rounds, with the amounts concentrated around the “1 billion yuan” mark, forming an unusually consistent threshold.

What does this mean? This means that before reaching 1 billion yuan, the financing market for embodied intelligence is a vibrant and diverse landscape; however, once it enters Series B, the rules suddenly shift to “large-scale concentrated betting”: venture capitals are only willing to allocate funds to a select few companies that can truly support engineering and mass production.

Behind this apparent disparity lies a signal that the industry is entering its next phase.

2. Why has “1 billion yuan” become a basic threshold?

To understand the rationale behind the 1 billion yuan threshold, we must first examine where the money before Series B was spent.

In the angel and Series A rounds, the main tasks for embodied intelligence companies are to define their technological roadmap, build prototypes, and assemble a functional team.

The company needs to prove two things: first, that the roadmap is physically feasible; and second, that it can be integrated with large models at the algorithmic level, demonstrating sufficient “plasticity.” Funds flow more towards algorithm talent, early hardware prototyping, and a small number of pilot projects,which is costly, but still within manageable limits.

By Series B, the tasks have fundamentally changed. A typical embodied intelligence enterprise at this stage faces several costly fronts simultaneously:

First, the engineering of the entire machine. Joints, motors, electric drives, sensors, and reducers—each component must move from “laboratory level” to “mass-producible level,” involving extensive reliability testing and supply chain collaboration.

Second, continuous investment in software and computing power. More modalities and larger models place higher demands on data closed-loop capabilities and inference deployment.

Third, building production lines and delivery systems. From production line processes and quality control to after-sales maintenance, any weakness in any link can be amplified into cost or security issues.

Simply put, before Series B funding, the company answers “Can we make it?”; after Series B, the company answers “Can we deliver it stably and on a large scale?” The former can be solved through clever engineering and temporary patchwork solutions, while the latter is a continuously costly systems engineering project.

Given this cost structure, is 1 billion yuan an exaggerated figure?

From the absolute value of a single round of financing, it’s certainly “frightening”; but if you break it down into R&D, production line, and scenario verification expenditures over the next two to three years, and consider the probability of failure, it’s actually just a basic threshold.

It’s more like venture capitals’ estimation of the “engineering window”: giving the company 24-36 months to simultaneously push the product, supply chain, and scenario to a replicable state; otherwise, it’s difficult to secure another round of larger-scale funding.

Because of this, venture capitals’ tolerance for error drops significantly in Series B funding. They are no longer willing to accompany companies in a “small steps, quick progress” approach, but rather prefer to use large-scale financing to compress time.

This is also why a gap appears in the Series B stage: it’s not that there’s no money, but that there are only so many institutions willing to write a 1 billion yuan “check.”

3. Three “Strange” Phenomena Point to the Same Contradiction

When 1 billion yuan becomes the threshold for Series B, some phenomena that seem a bit “contradictory” to outsiders become easier to understand.

The first phenomenon is the misalignment between valuation and financing pace.

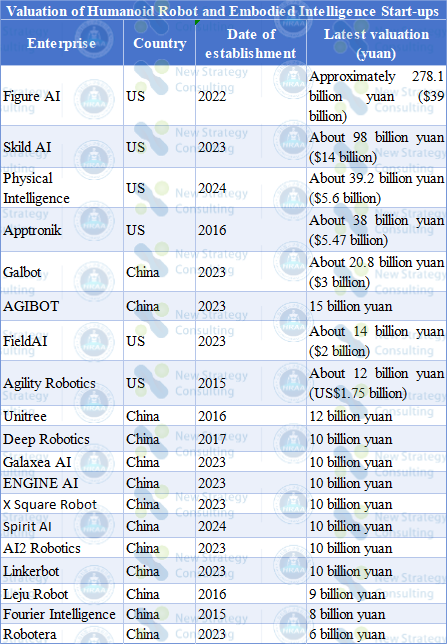

Looking at valuation tables, Figure’s valuation is approaching $39 billion, while Skild AI, Physical Intelligence, Apptronik, and FieldAI are all in the billions of dollars. Domestically, Galbot is valued at approximately $3 billion, while AGIBOT and Unitree are valued at around $2 billion. The latest valuations of companies like Deep Robotics, Galaxea AI, Engine AI, X Square Robot, Spirit AI, AI2 Robotics, and Linkerbot are generally around 10 billion yuan.

In other words, valuations in the tens of billions of yuan are no longer uncommon in this sector. When valuations reach such heights, the next round of financing becomes delicate: new investors must accept an already expensive starting point and bear the risks of uncertainty in engineering and commercialization.

As a result, some companies, with high valuations, find it extremely difficult to advance the next round of financing, and may even have to consider “circumventing the system” by establishing new project companies or spinning off a specific technology or application line for separate financing, allowing venture capitals to enter from a relatively clean new entity with a lower valuation base.

The second phenomenon is the change in capital structure behind Series B financing.

The table shows that investors in leading overseas companies are almost exclusively tech giants and top-tier dollar funds: industry players like Nvidia, Microsoft, Amazon, and Samsung are betting alongside financial investors like CapitalG and Thrive Capital.

Domestically, the picture is different: industrial capital from companies like CATL, Baidu, Meituan, TCL, and CRRC is appearing alongside institutions like CICC Capital, CDB Venture Capital, and local state-owned capital funds, indicating a clear industry synergy and policy guidance.

This means that companies reaching the 1 billion yuan mark are rarely just receiving “purely financial hot money.” They are often simultaneously categorized into specific industry camps: battery and energy storage, complete vehicles and autonomous driving, industrial automation and manufacturing, and city-level infrastructure.

The other side of money is scenarios, supply chains, and resources. In this structure, the competition in Series B funding is no longer about “who makes the robot’s movements smoother,” but rather “who can embed themselves into a more diverse and stable industrial system.”

The third phenomenon is the emotional split surrounding the industry tracks.

On the one hand, new financing news keeps emerging, and valuations continue to climb, seemingly propelling everything towards the “next-generation platform.”

On the other hand, pessimistic voices exist within the industry: some directly question whether humanoid robots will become an “industry driven by financing.” After all, compared to other sectors, truly large-scale deployments and stable cash flow are still limited, and unit costs, maintenance costs, and reliability are still being continuously adjusted.

These two sentiments essentially stem from the same contradiction: the sector has reached the “late-stage funding” level at the capital level, but at the industrial and commercialization level, it remains in the early to mid-stages. The 1 billion yuan Series B round is both the ammunition needed to bridge the engineering gap and an amplifier amplifying this misalignment.

4. What’s more noteworthy after the 1 billion yuan threshold?

If we take a longer view, the 1 billion yuan threshold is neither the end nor a simple bubble label, but rather a signal that embodied intelligence is moving from a “hotspot” to a “survival of the fittest.”

From a financial perspective, the 1 billion yuan Series B round divides the sector into two worlds.

In one world, a select few companies, backed by industry giants and state-owned capital, have secured enough funding to support 2-3 years of engineering and mass production investment, allowing them the opportunity to experiment with different scenarios and business models.

In another world, a large number of companies remain in the Series A and Pre-A stages, with funding primarily for survival. They struggle to sustain long-term, asset-heavy experiments and are therefore more likely to be eliminated or merged into leading players.

From an industry perspective, as the barriers to entry rise, the industry is also forced to answer several more specific questions:

First, when will we see truly standardized products, rather than one-off demo projects?

Second, in which industry scenarios can humanoid robots and embodied intelligence truly achieve positive unit economics, rather than merely serving as vanity projects?

Third, can safety, reliability, and operational costs be controlled and predicted, rather than requiring a complete re-engineering process for each project?

From an observer’s perspective, in the next year or two, what’s perhaps more noteworthy isn’t how many new funding rounds there are or what records are broken, but rather whether these companies that have already crossed the 1 billion yuan threshold can provide verifiable answers in engineering and commercialization.

If these answers gradually emerge, the seemingly exaggerated 1 billion yuan figure today will prove to be merely a “re-equipment” before embodied intelligence matures; if it doesn’t materialize for a long time, those dazzling funding rounds and valuations will inevitably be repriced.

In 2026, the embodied intelligence industry stands at this watershed: on one side, a constant barrage of funding news; on the other, the ongoing progress of engineering and commercialization.

The 1 billion yuan Series B threshold makes this dividing line exceptionally clear. The real test isn’t in the news, but in the next two or three years.