The listing of LDROBOT on the Stock Exchange of Hong Kong (HKEX) was like a pebble thrown into a long-calm lake.

On May 11, 2026, LDROBOT, Shenzhen-based company, officially listed on the main board of the HKEX, opening more than 100% higher than its issue price and closing with a gain of 127.62%, pushing its total market capitalization above HK$20 billion. Even more noteworthy was the overwhelming demand for LDROBOT’ IPO, with its Hong Kong public offering oversubscribed by 6707.66 times, one of the highest oversubscription rates for Hong Kong IPOs this year, and the international placement also achieving 9.54 times oversubscription.

The capital market never lies. The 6707-fold oversubscription reflects the long-accumulated imagination of the entire lawnmower robot sector in the minds of institutional and retail investors. LDROBOT’ listing was merely the spark that ignited the fuse.

1. Where will hot money be poured into this sector during its window of opportunity?

Before understanding this round of capital enthusiasm, it’s necessary to return to the market itself. The influx of capital is never aimless; it stems from a precise prediction of industry trends.

Statista data shows that there are approximately 250 million private gardens globally, with Europe and the US accounting for over 70%, while the overall penetration rate of robotic lawnmowers is less than 6%. This contrasts sharply with the 16 million push robotic lawnmowers shipped globally annually. High labor costs for maintenance in Europe and the US, coupled with the continued maturation of battery and AI navigation technologies, are accelerating this category’s transition from a niche market to the mainstream. High ceilings and low penetration rates—the structural opportunities inherent in the sector are the most compelling reason for capital investment.

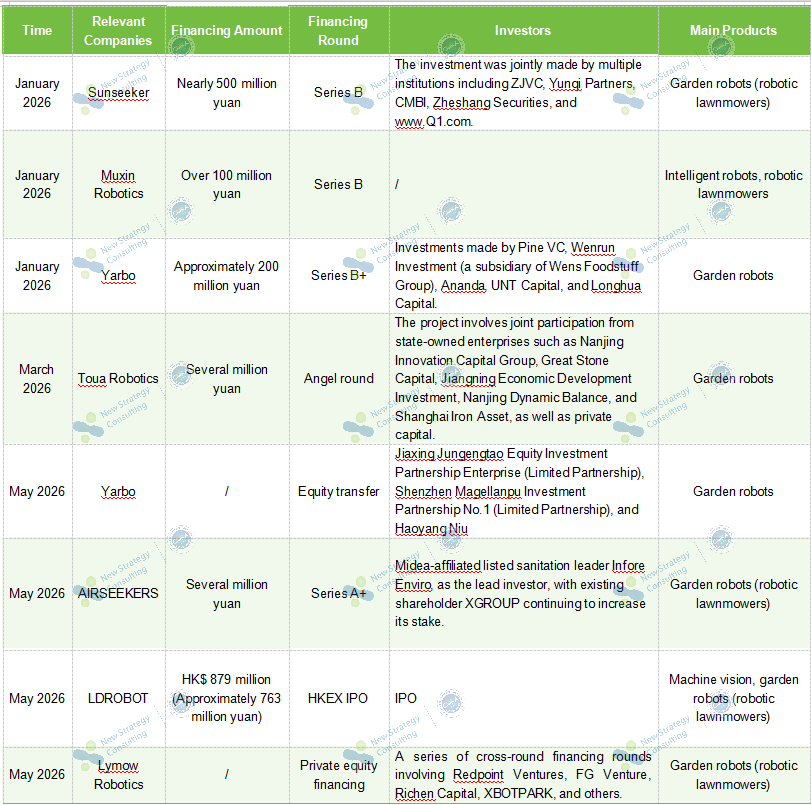

Capital sensed this opportunity even before the industry itself. This expectation quickly transmitted to the primary market and is clearly reflected in subsequent financing data. From the beginning of 2026 to the present, in just five months, the robotic lawnmower sector has seen several rounds of financing, accumulating over 1.6 billion yuan, signaling that the industry is transitioning from the “validation phase” to the “scale-up phase.”

Chart: Overview of Funding in the Robotic Lawnmower Sector as of May 2026

In January, Sunseeker, the established player, completed a nearly 500 million yuan Series B funding round, with joint investment from multiple institutions including ZJVC, Yunqi Partners, CMBI, and Zheshang Securities. As a leading domestic garden equipment manufacturer with over a decade of experience in the European market, this round of financing clearly targets “deep penetration into overseas markets” and “upgrading of its full-scenario product matrix.”

Meanwhile, Muxin Robotics announced the completion of a over 100 million yuan Series B funding round, with the funds primarily used for the R&D of its next-generation four-wheel drive products and channel expansion. Notably, in 2021, Muxin Robotics officially launched its robotic lawnmowers project and has established a deep strategic partnership with consumer electronics giant Anker. Its eufy robotic lawnmowers series has already demonstrated strong channel penetration in the European and American markets.

Also in January, Yarbo completed a approximately 200 million yuan Series B+ funding round, attracting leading financial investment institutions, listed company industrial capital, and local government-guided funds. Among them, Wenrun Investment (backed by Wens Foodstuff Group) is expected to provide synergy in supply chain optimization, manufacturing, and channel expansion; Ananda, as a listed company in the motor drive field, will enhance Yarbo’s vertical integration capabilities in core power components; and UNT Capital will provide industrial support in underlying technologies such as chips and electronic controls. It is understood that the funds raised in this round will mainly be used to deepen technology research and development, accelerate product iteration, and expand market channels.

Entering March, early-stage projects began to emerge. Toua Robotics completed a tens of millions of yuan angel round of financing, with participation from multiple state-owned and social capital entities in Nanjing. The funds will be used for the research and development and production of intelligent robotic lawnmowers and pool cleaning robots.

Since May, the pace of financing has further accelerated. AIRSEEKERS completed a tens of millions of yuan Series A+ round of financing, led by Midea-affiliated listed sanitation leader Infore Enviro, with existing shareholder XGROUP continuing to invest. AIRSEEKERS has focused this round of financing on three directions: iteration of core technologies such as borderless navigation and lightweight obstacle avoidance, expansion of its product matrix, and improvement of its supply chain and channels in the European and American markets. The entry of Infore Enviro is particularly noteworthy. This listed company, deeply rooted in B2B municipal sanitation, has chosen this time to bet on C2C home and garden robots, demonstrating a clear logic of industrial synergy: covering the entire outdoor intelligent scenario from municipal to garden applications.

In the same month, Yarbo also underwent a change in shareholding, continuing to attract capital investment. Furthermore, Lymow Robotics completed a private equity financing round at the end of the month, with Redpoint Ventures, FG Venture, Richen Capital, and XBOTPARK participating in a cross-round financing. Lymow Robotics focuses on the R&D of robotic lawnmowers, and its products have entered multiple markets in North America and Europe. This round of financing will further support its overseas expansion.

Besides private equity financing, companies in the sector have also begun raising funds through the public market, with LDROBOT being a prime example. Through its IPO on the HKEX, it successfully raised HK$879 million, which will be primarily invested in the continued R&D of visual perception and robotic lawnmower technologies, brand building, and channel development. Simultaneously, it will advance the construction of new R&D centers in Beijing and Shenzhen, providing ample momentum for the company’s long-term development and becoming another important signal of the sector’s large-scale development.

Analyzing the investment destinations of this round of financing reveals three clear common themes: continuous investment in technological research and development (especially borderless navigation and AI obstacle avoidance), expansion of the product matrix from single lawnmowing to all-around garden scenarios, and a strong emphasis on channel development in the European and American markets. These three themes also represent the three core dimensions that determine success or failure in this sector.

2. The battle for the “first stock” has begun

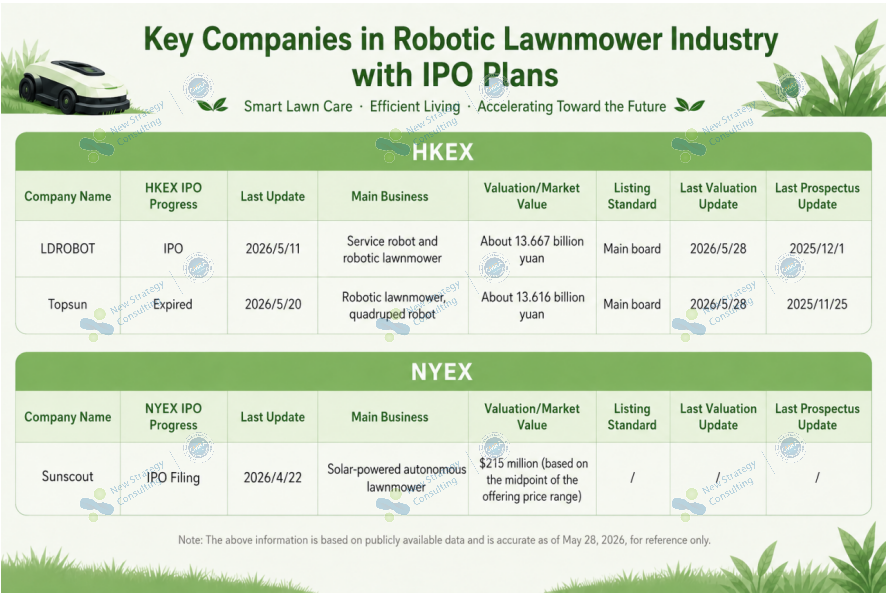

Beyond financing, another narrative thread is also progressing simultaneously in the robotic lawnmower sector—IPOs.

In May of this year, LDROBOT fired the first shot. A closer look at its business structure reveals that LDROBOT follows a typical “dual-track” approach. On one hand, since 2018, LDROBOT has focused on DTOF lidar and SLAM algorithms, providing core perception components to manufacturers of robotic vacuum cleaners and commercial service robots. On the other hand, since 2022, LDROBOT has been extending downstream into complete machine manufacturing, with robotic lawnmowers becoming a key area for accelerated growth.

According to LDROBOT’ financial report, in 2024, revenue from its robotic lawnmower business was 23.272 million yuan, accounting for only 5% of total revenue. By 2025, this proportion had expanded to 18.3%, recording revenue of 136 million yuan. Although the 18.3% revenue share means that robotic lawnmowers have not yet become a core business, LDROBOT’s IPO still has significant breakthrough significance in this sector: the 6707-fold oversubscription proves that the robotic lawnmower narrative is enough to generate such a strong response in the capital market.

And LDROBOTng is not the only participant in this positioning battle.

One is Topsun, already listed on the A-share market and currently applying for a Hong Kong IPO. In November 2025, it planned to use the raised funds for the industrialization of quadruped robots, the upgrading of intelligent robotic lawnmowers, and the expansion of its production base, relying on a dual-path development strategy of “traditional garden machinery + intelligent transformation.” The company has a high proportion of revenue from the European and American markets, and its mature channels accumulated over two decades can significantly reduce customer acquisition costs, forming a barrier that is difficult for competitors to replicate. However, in April 2026, according to public information, the company was investigated by the China Securities Regulatory Commission (CSRC) for suspected information disclosure violations and received a warning letter. On May 25, its Hong Kong IPO prospectus automatically expired after six months without a hearing, and the A+H listing process was temporarily suspended. As of now, the company has not submitted a renewal application. Topsun‘s robotic lawnmower and quadruped robot businesses remain its core strategic focus, but the progress and pace of the capital market will need to wait for the compliance issues to be clarified before restarting.

Another company is Sunscout, a New Zealand company. It has officially submitted its IPO application to the New York Stock Exchange (NYSE), focusing on solar-powered autonomous lawnmowers, with a median offering price corresponding to a valuation of approximately US$215 million. With solar energy as a differentiated entry point and targeting the North American market, Sunscout has a clear technological path and niche positioning. However, the penetration rate of lawnmowers in North America is still less than 5%, and market education costs are high. Whether Sunscout can gain Wall Street’s valuation approval remains to be seen.

Looking at the three companies, their processes and paths differ, but they share a striking similarity: robotic lawnmowers are not their absolute core business. Even so, their efforts to enter the capital market are continuously accumulating attention and market depth for this sector. Therefore, the true suspense surrounding the “first stock” in this sector remains unresolved.

Currently, companies deeply focused on lawnmowers, such as Sunseeker, Muxin Robotics, Yarbo, and Mammotion, which have completed multiple rounds of capital investment and are not yet publicly listed, are key players in the future landscape of the industry. Their subsequent development deserves long-term monitoring.

3. A million-unit tier has emerged, and new players are rapidly reshaping the landscape

Of course, regardless of financing or IPOs, the confidence behind the capital narrative ultimately rests on the product itself. Where does the money in the primary market flow, and how is the story told in the public market, the underlying support is the same question: how many robotic lawnmowers have actually been sold in the global end-user market?

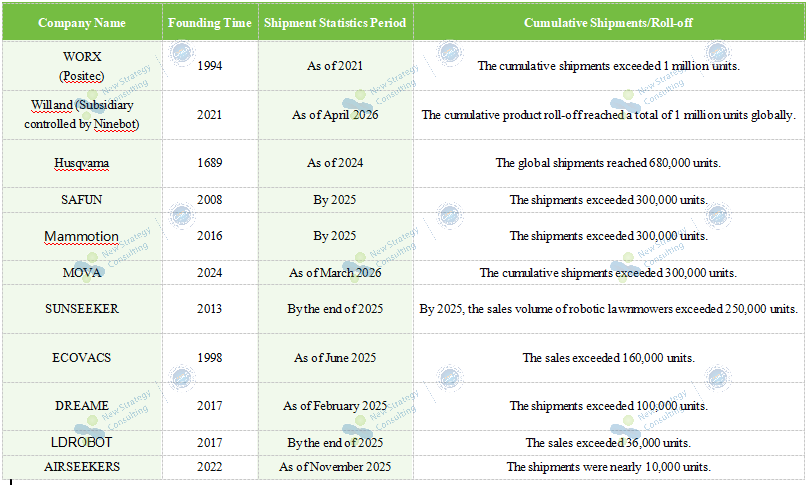

Market growth is already speaking for itself in the data. According to IDC data, global shipments of robotic lawnmowers reached 1.992 million units in 2025, a year-on-year increase of 63.8%, making it the fastest-growing segment among all intelligent robot subcategories. More noteworthy is the dramatic shift in the internal structure: shipments of borderless robotic lawnmowers reached 1.318 million units, a surge of 182.4% year-on-year, jumping to 66.2% of the market share and completely replacing wire-laying models as the mainstream.

This shift in mainstream means that old competitive barriers are being broken down, and a new landscape is yet to take shape—and in this reshuffling process, the shipment data of various companies are already beginning to outline the future.

Chart: Overview of Shipments by Some Robotic Lawnmower Companies

*The shipment data in this article is mainly based on company disclosures. Different companies may have different statistical methods for “shipments,” “deployment,” and “product rolloff“; and some companies have not disclosed specific shipment data and are therefore not included in the statistics.

Currently, the industry has seen the emergence of two companies with shipments exceeding one million units, forming a differentiated pattern of “established deep-rooted players + cross-industry newcomers.”

WORX, a subsidiary of Positec, is a veteran player in the industry. Leveraging 30 years of technological expertise and overseas channel accumulation, its cumulative shipments exceeded one million units in 2021, once holding a dominant market share in key European markets such as Germany, France, and Italy. This is a barrier built over time and through channel development.

Similarly, Willand, a subsidiary of Ninebot established in 2021, has also surpassed one million units globally by April 2026. Reaching the million-unit mark in just five years is attributed to Ninebot’s dual-brand strategy in the European and American markets, as well as the direct reuse of channel and supply chain resources in the smart mobility sector.

Meanwhile, domestic Chinese brands are collectively making strides, achieving large-scale breakthroughs in overseas markets and building a solid competitive advantage. In 2025, SAFUN and Mammotion both surpassed 300,000 units shipped, establishing a foothold in mainstream European and American markets. MOVA, a startup founded in 2024, has experienced remarkable growth, shipping over 300,000 units by March 2026, achieving a breakthrough from zero to 300,000 units in just two years. This speed is rare even within the entire consumer electronics industry, demonstrating the maturity of its seamless robotic vacuum cleaner technology, significantly shortening the scaling cycle for new players, and proving that cross-border e-commerce channels can efficiently empower new brands, confirming that the sector still has huge growth potential.

Many cross-industry companies and emerging brands continue to unleash their growth momentum. Sunseeker‘s sales exceeded 250,000 units in 2025, while simultaneously completing a nearly 500 million yuan Series B financing round. The increased investment from the capital market fully recognizes the sustainability of its scaled growth. Ecovacs and Dreame, leveraging their technological and channel accumulation in the robotic vacuum cleaner field, have entered the market with outstanding performance. As of June 2025, Ecovacs’ sales exceeded 160,000 units; as of February 2025, Dreame’s shipments exceeded 100,000 units. Furthermore, LDROBOT‘ sales reached 36,000 units in 2025, nearly tripling compared to 2024, which is also a core reason for its exceptionally high subscription rate in the capital market.

In summary, this shipment volume chart conveys several noteworthy signals.

Firstly, industry concentration is still low, with both companies in the million-unit tier and emerging players in the tens of thousands-unit tier coexisting. Newcomers still have room to catch up, and the market is far from a winner-takes-all stage. Secondly, Chinese brands are systematically rising. From Willand, Mammotion, and MOVA to Sunseeker, Chinese companies are present at every level of the industry, reshaping the global competitive landscape. Thirdly, the positive correlation between shipment volume and financing scale is becoming increasingly apparent. Whoever can achieve a leap in scale first will have stronger pricing power in the next round of financing or IPO.

Currently, the robotic lawnmower industry has officially entered the era of tens of thousands of units in scale. Industry reshuffling continues, and the competition among major brands for a new round of sales growth has fully commenced.