On April 1, the 4th Conference on the Promotion of the Commercial Application of Unmanned Cleaning & Sanitation Robots 2026, jointly hosted by China Low-Speed Automated Driving Industry Alliance (LSAD) and China Clean Expo (CCE), and exclusively sponsored by Jinlv Environmental Technology Co., Ltd., was successfully held in Shanghai.

The conference focused on the innovative development of property cleaning robots and the large-scale application of municipal sanitation robots, which brought together core industry players including vehicle and solution providers, core technology suppliers, sanitation operators, and city service companies, attracting over 400 attendees to explore technological innovation and commercialization pathways.

Simultaneously, the conference was streamed online with photos, attracting nearly 30,000 viewers and generating enthusiastic responses.

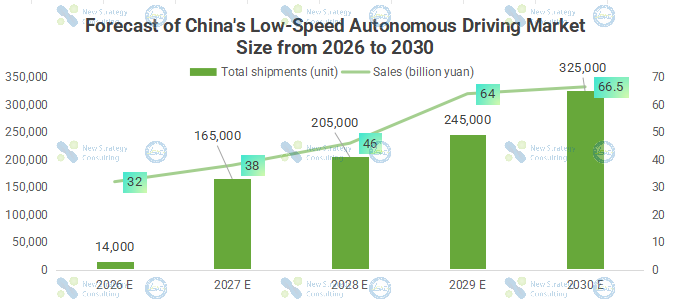

At the conference, LSAD and New Strategy Low-Speed Automated Driving Industry Research Institute released the 2025-2026 Chinese Low-speed Autonomous Driving Industry Development Report, and shared relevant data and market demand analysis in the field of autonomous sanitation.

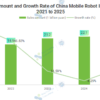

At the launch event, Li Jinke, Secretary-General of LSAD and Director of New Strategy Low-Speed Automated Driving Industry Research Institute, provided an in-depth analysis of the report’s core data. He pointed out that in 2025, the total shipments of various low-speed autonomous driving equipment in China exceeded 68,000 units, a year-on-year increase of approximately 106%; sales reached approximately 21.4 billion yuan, a year-on-year increase of approximately 91%, reflecting the industry’s leapfrog growth from the technology verification stage to the large-scale commercial application stage.

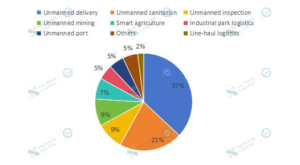

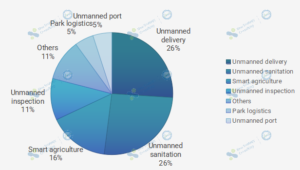

In terms of scenario structure, the top three sub-sectors in terms of shipment volume were unmanned delivery, unmanned sanitation, and unmanned shuttle services, while the top three in terms of sales volume were unmanned mining, unmanned delivery, and unmanned shuttle services. Among these, the unmanned delivery industry performed particularly well, with shipments of approximately 42,000 units and sales of approximately 4.9 billion yuan in 2025, becoming the first hot sector in the low-speed autonomous driving field to achieve tens of thousands of units deployed in a single year.

With continued strengthening of policy support, increasingly improved supply chain, and gradually clearer business models, the low-speed autonomous driving industry is ushering in a golden age of development.

LSAD and New Strategy Low-Speed Automated Driving Industry Research Institute predict that the sales of low-speed autonomous driving equipment in China will reach 32 billion yuan in 2026, with shipments expected to increase to 140,000 units.

Li Jinke further pointed out that there are currently nearly 3,000 companies related to the autonomous driving industry chain in China, of which more than 450 are representative companies focusing on the manufacturing of various low-speed autonomous driving equipment and overall solutions. Autonomous driving and robotics companies account for approximately 55%. In terms of penetration, autonomous driving technology companies have a deeper presence and higher market share in sanitation, delivery, and shuttle services.

With the accelerated entry of operation service providers and traditional OEMs into multiple scenarios, future industry competition has shifted from a single product technology contest to a comprehensive strength competition encompassing cost control, operational efficiency, and full lifecycle service capabilities. In this process, companies with a deep understanding of scenarios, supply chain integration capabilities, and commercialization experience are more likely to take the initiative in the next round of industry reshuffling.