In early 2026, the global autonomous driving industry saw accelerated capitalization.

On January 29, Boonray formally filed its prospectus with the Stock Exchange of Hong Kong (HKEX), marking the start of its listing journey on HKEX as a pure electric autonomous mining truck provider. On March 5, market reports revealed that autonomous driving technology company Momenta had secretly submitted an IPO application to the HKEX, aiming to raise at least $1 billion.

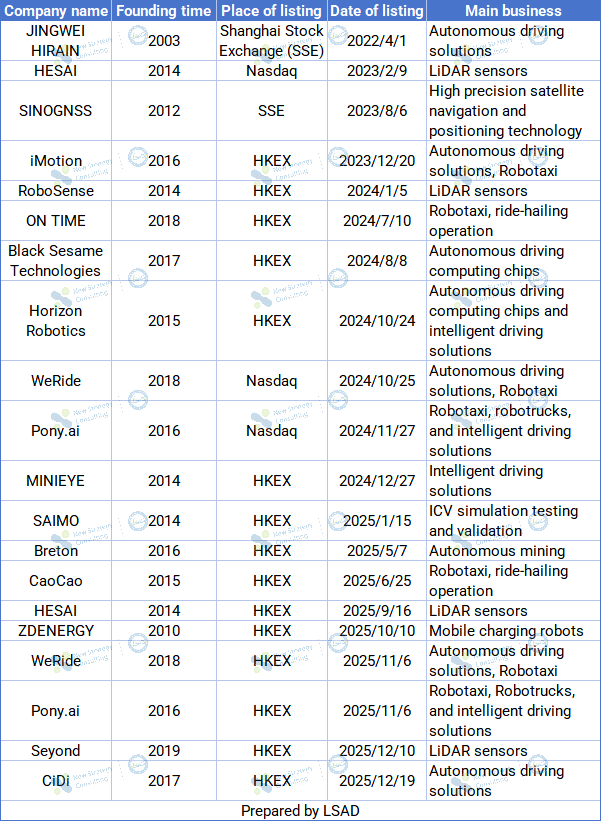

According to incomplete statistics from China Low-speed Automated Driving Industry Alliance (LSAD), as of March 9, 2026, over 30 companies in the autonomous driving industry chain have submitted applications or successfully gone public. Among them, 17 companies have completed IPOs, 2 companies have terminated their IPO processes, and 11 companies are in the stages of filing for listing or filing.

Overview of Listed Autonomous Driving Companies in China

Among listed companies, 14 have chosen to be listed on the HKEX, with their proportion notably increasing after 2024. This reflects the strong appeal of HKEX in valuing and supporting the liquidity of autonomous driving technology firms. Meanwhile, Nasdaq and SSE offer diversified capital channels. Companies like HESAI, WeRide, and Pony.ai have even adopted dual listings on both Nasdaq and HKEX to optimize capital structures, demonstrating how the industry is leveraging global capital markets to accelerate expansion.

The distribution of core business operations reveals that listed companies now span the entire industrial chain, from foundational hardware and core technologies to scenario-based operations. Notable examples include LiDAR firms HESAI, RoboSense, and Seyond; chip R&D and manufacturing leaders Black Sesame Technologies and Horizon Robotics; high-precision navigation provider SINOGNSS; and autonomous driving solution providers JINGWEI HIRAIN and iMotion. This demonstrates that investors are not only pursuing technological breakthroughs but also actively supporting commercialization. The recent listings of companies like Breton (an autonomous mining solution provider), CiDi, and ZDENERGY (a mobile charging robot service provider) underscore the industry’s transition from technical validation to large-scale application, with capitalization progress closely paralleling industrial maturity.

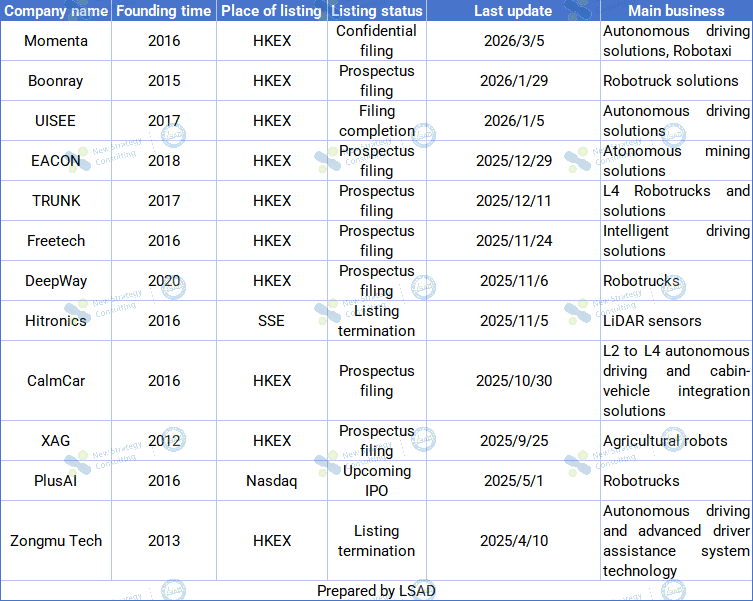

Overview of the IPO Progress of Autonomous Vehicle Companies in Major Stock Exchanges in China

HKEX has also emerged as the preferred listing destination for most companies in their IPO push. According to data from LSAD, among the 10 companies still in the queue at major exchanges, nine are targeting the HKEX, while only PlusAI plans to list on NASDAQ.

In terms of industry sectors, companies in the queue are highly concentrated in commercial vertical applications, particularly in high-frequency, essential sectors with closed or semi-closed environments. From late 2025 to early 2026, autonomous mining firms like EACON and Boonray filed applications for listing on the HKEX. Meanwhile, UISEE completed its filing in early January for unmanned airport operations, with the listing process accelerating steadily.

Conclusion:

The presence of over 25 autonomous driving companies listed on HKEX demonstrates that international investors have established a stable valuation framework and exit strategy for this sector. Meanwhile, capital is pouring into vertical applications like mining, ports, and logistics—sectors that can rapidly validate economic value—whether through established players like Breton or emerging entrants such as Boonray, EACON, and WestWell. This marks a clear signal that the public market is awarding ‘graduation certificates’ to companies that have moved beyond technical demos and entered large-scale commercial operations, backed by tangible financial investments.

Looking ahead, this capitalization process will profoundly reshape the industry landscape. On one hand, companies that successfully go public will gain ample resources for technological iteration, market expansion, and global competition, accelerating industry consolidation and the Matthew effect. On the other hand, the industry’s competition is shifting from laboratory-level technological contests to a race for commercialization and operational efficiency fueled by capital markets. The autonomous driving narrative has finally turned a new page, with revenue and profit becoming the core focus.