In recent years, advancements in AI, 5G, and other technologies have positioned autonomous driving as a key trend in the automotive industry. Traditional commercial vehicle manufacturers, facing rising labour costs, shifting market demands, and intense competition, are under immense pressure to find new growth avenues. Many are turning to autonomous driving, investing heavily in the sector to stay relevant and sustainable.

Transitioning to Autonomous Driving

The era of smart and new-energy vehicles has not only redefined product functionality and business models but also reshaped industry boundaries and disrupted the automotive supply chain. These changes have lowered the barriers to entry for new players. In response, traditional manufacturers have pivoted toward autonomous driving, leveraging both independent R&D and partnerships with startups.

For instance, Beiqi Foton Motor began developing autonomous driving in 2015 and now covers logistics, sanitation, and last-mile delivery. Its subsidiary Foton Loxa, established in 2020, focuses on lightweight, smart, and new-energy vehicles. Similarly, FAW Jiefang’s Zhito Technology has developed autonomous solutions for sanitation and has moved to commercialization.

In the port automation space, ZPMC has deployed autonomous vehicles in several ports, including Tangshan and Guangzhou. Xuzhou Construction Machinery Group (XCMG) has introduced autonomous mining trucks like the XDE240 and the XDR80TE-AT, which are already operational at several major mining sites. Other major players, such as Weichai, Inner Mongolia North Hauler, and Tonly Heavy Industries, have also launched autonomous vehicles for mining, capitalizing on high labour costs and safety concerns in the sector.

Traditional agricultural machinery manufacturers have also entered the autonomous technology race. Companies like Zoomlion, Weichai Lovol, and YTO Group are innovating in smart farming with autonomous harvesters, tractors, and precision farming platforms.

In the autonomous shuttle space, major bus manufacturers such as Dongfeng, King Long, Zhongtong, and Yutong have developed driverless bus models. However, transitioning to autonomous driving poses challenges, including keeping up with rapid technological advances and aligning with market demand.

Despite efforts to embrace autonomous and new-energy trucks, SAIC Hongyan filed for bankruptcy restructuring in October. The company pioneered “5G+L4” autonomous heavy-duty trucks and introduced a full lineup of pure electric trucks. However, sluggish demand for heavy-duty vehicles and mounting financial losses led to its downfall.

From January to September 2024, SAIC Hongyan sold just 5,531 trucks, far below its target of 30,000 units. Legal troubles further worsened its financial position, with $526 million in funds frozen by courts. Its parent company, Shanghai New Power Automotive Technology, has incurred losses of $470 million since 2022, leaving it unable to provide further financial support.

Increasing Market Consolidation

Both traditional manufacturers and autonomous startups face similar challenges in achieving commercialization and financial self-sustainability. Recent industry developments highlight these struggles:

Autra Tech, an autonomous trucking company, has begun bankruptcy proceedings after downsizing and cutting salaries.

ZongMu Technology, once a star in autonomous driving, recently reduced wages to basic living expenses amid financial struggles.

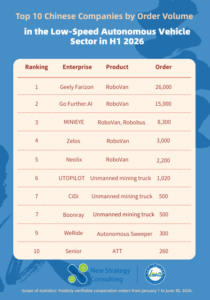

Other companies, such as Qingtian Truck and TuSimple, have also faced bankruptcy or delisting. Meanwhile, firms like WeRide, Pony.ai, and MINIEYE are turning to IPOs for survival.

Outlook

The autonomous driving industry remains a high-risk, capital-intensive field. Companies with weak revenue streams or limited investor interest are being eliminated, and this trend of market consolidation shows no signs of slowing down. Only those capable of sustaining innovation and adapting to market realities are likely to thrive in the long term.