The year of 2025 is hailed as the “inaugural year” for autonomous delivery vehicles in the industry. With strengthened policy support and continuously declining technology costs, the sector is transitioning from technical validation to large-scale commercial operations. According to the latest data from Low-Speed Automated Driving Industry Alliance (LSAD), the Chinese autonomous delivery industry is expected to ship approximately 42,000 low-speed autonomous driving units in 2025, marking a year-on-year increase of over fivefold.

With the market boom, the unmanned delivery sector has witnessed fiercer competition and consolidation. According to incomplete statistics from LSAD, since 2025, over 15 Chinese companies have entered the unmanned delivery arena, either as new entrants, cross-industry players, or companies expanding their operations into this field.

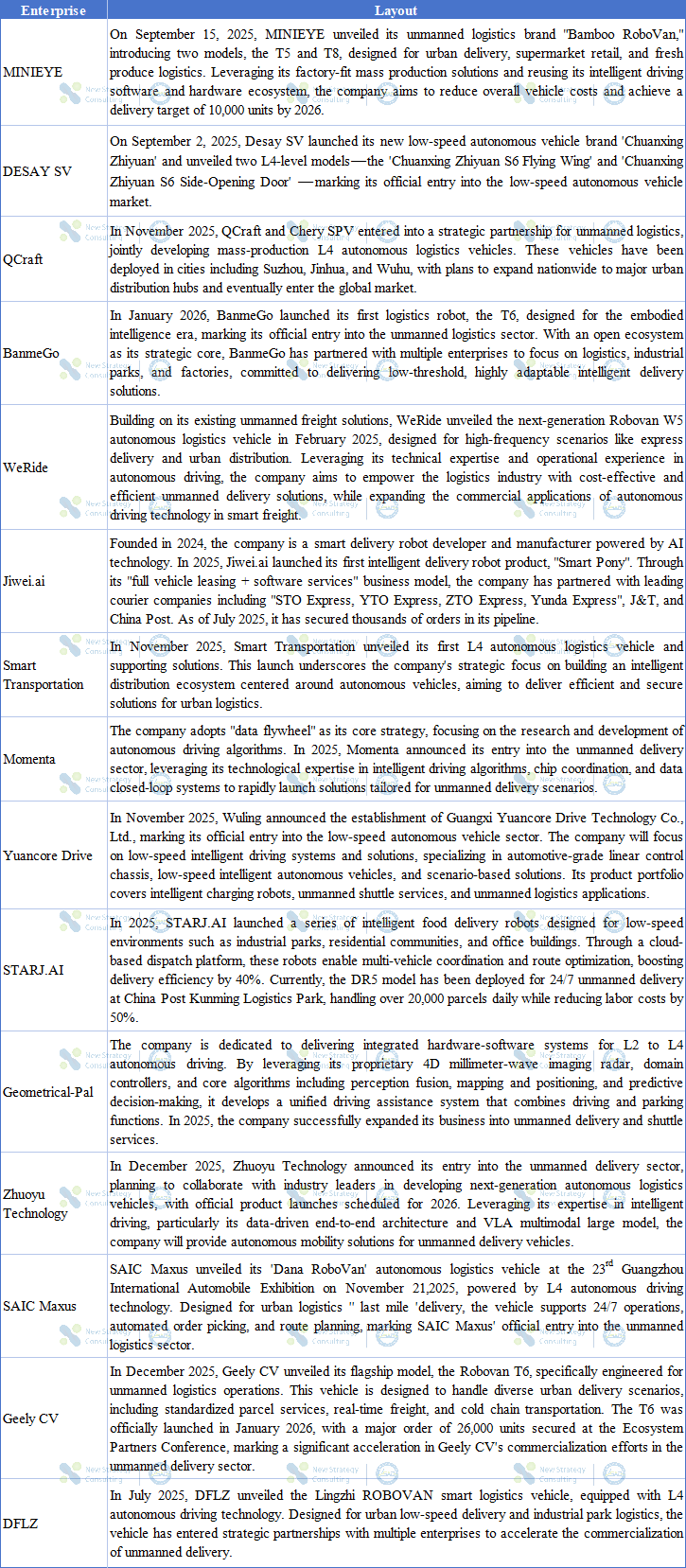

Companies Set to Enter the Unmanned Delivery Sector in 2025

Beyond the aforementioned automakers, several other major manufacturers, including Xiamen King Long, Dongfeng Motor, Chery Automobile, JAC Motors, and New Gonow Recreational Vehicles, have recently launched their own or co-developed autonomous delivery vehicles.

Unmanned Delivery Opens a Chapter of Multiple Narratives

The influx of numerous companies into the unmanned delivery market is undoubtedly a natural outcome of its explosive growth. At a deeper level, it reflects the broader shift of autonomous driving technology from laboratory testing and factory-fit systems in passenger vehicles to large-scale commercial applications.

Among them, high-end intelligent driving technology companies like MINIEYE, QCraft, WeRide, and Geometrical-Pal can leverage their existing “intelligent driving software and hardware ecosystems” to achieve horizontal expansion of their technology platforms. This approach significantly reduces vehicle costs and shortens R&D cycles. By identifying more commercially viable sectors beyond passenger vehicles, they can rapidly monetize their technologies.

Traditional automakers and component giants like DESAY SV, SAIC Maxus, Geely CV, and Yuancore Drive have made strong inroads into the market with their deep expertise in vehicle engineering, supply chain management, and automotive-grade manufacturing. Their products often boast inherent advantages in reliability, mass production consistency, and cost control, aiming to carve out new growth trajectories amid the automotive industry’s intelligent and electrified transformation.

Furthermore, emerging tech companies like BanmeGo, Jiwei.ai, and Smart Transportation, along with cross-industry players, prioritize market entry through innovative approaches. For instance, BanmeGo emphasizes “embodied intelligence” and open ecosystems, while Jiwei.ai adopts a streamlined “vehicle leasing/software services” model to partner directly with major courier providers. Smart Transportation leverages its telecom operator background to build an intelligent delivery ecosystem. These players sidestep direct hardware competition with traditional players, establishing differentiated advantages in niche scenarios or service offerings through business model innovation, ecosystem development, or cutting-edge technology integration.

As we can see, the new entrants in the unmanned delivery sector by 2025 are no longer limited to proof-of-concept stages. Equipped with mature technological modules, clear business models, and concrete mass-production targets, they are directly targeting rapidly commercializable scenarios such as express delivery, urban distribution, retail, and industrial parks. With their innovative technological frameworks and engineering capabilities that have been extensively validated, these players are fundamentally transforming the unmanned delivery industry from a ‘Demo-driven’ phase to a new era of ‘supply chain-driven’ and ‘data-driven’ development.

Who can outshine the rest?

In 2025, the entry of new players including tech firms and traditional automotive supply chain giants has disrupted the competitive landscape between the “technology startup faction” represented by Neusoft’s autonomous vehicles, Jiushi, and White Rhino, and the “internet/logistics platform faction” represented by JD.com and SF Express. This shift has evolved into a complex ecosystem where four key players—technology solution providers, vehicle manufacturers, operational ecosystem operators, and terminal scenario partners—interpenetrate while competing and collaborating. This dynamic is propelling the industry from a “blossoming” exploratory phase into a new era, where core competitiveness lies in large-scale delivery capabilities, full-stack solution efficiency, and sustainable business models.

In this phase, the unmanned delivery sector will transition from competing on “single-point technologies” to vying for “systematic capabilities”. Diverse stakeholders are driving the industrial chain to evolve from a simplistic “vehicle manufacturing + algorithms” model toward more specialized divisions of labor. Meanwhile, the influx of numerous players is intensifying homogeneous competition, accelerating market fragmentation, and making the paths of scenario-specific development and scale expansion increasingly clear.

Going forward, in this new competitive landscape, how different types of enterprises leverage their unique strengths to achieve differentiated breakthroughs will be a key focus for the industry in the next phase.

In this evolution, the zero-sum logic is being replaced by a new paradigm of collaborative symbiosis. Whether it’s trailblazers dominating the top tier, industry giants controlling key scenarios, or emerging competitors with aggressive momentum, the key to success for all participants lies in building or deeply integrating into a robust industrial ecosystem.

The 4th Conference on the Promotion of the Commercial Application of Unmanned Cleaning & Sanitation Robot 2026 will be held by China Low-speed Automated Driving Industry Alliance (LSAD) on April 1, 2026 at Shanghai New International Expo Center. Stay tuned!