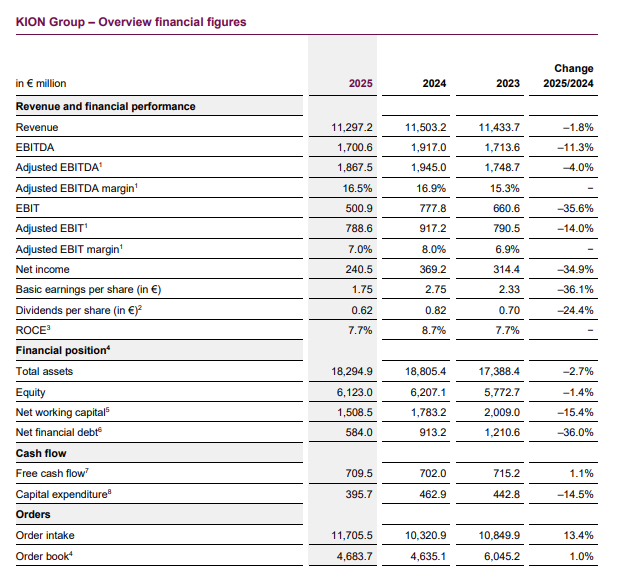

According to China Mobile Robot Industry Alliance (CMRA), on February 26 local time, KION Group officially released its 2025 Annual Report. The report shows that KION Group’s revenue for 2025 reached €11.297 billion, a decrease of 1.8% compared to €11.503 billion in 2024. Orders for 2025 reached €11.706 billion, an increase of 13.4% compared to €10.321 billion in 2024.

These data demonstrate that, in an industry environment characterized by macroeconomic fluctuations, supply chain restructuring, and automation upgrades, KION Group demonstrated its ability to weather economic cycles as a global leader through strong order growth, revenue resilience, optimized profit structure, and healthy cash flow.

I. Stable revenue, continuously optimized profit structure

In 2025, KION Group achieved operating revenue of €11.297 billion, a slight decrease of 1.8% year-on-year, maintaining overall stable growth. Revenue faced short-term pressure due to the return to normal delivery cycles, product structure, and pricing environment, but its scale remained firmly among the top tier globally.

Profitability: The Group’s adjusted EBIT was €788.6 million, corresponding to an adjusted EBIT margin of 7.0%; net profit was €240.5 million.

Structural highlights: The Supply Chain Solutions segment (renamed Intelligent Automation Solutions (IAS) from 2026) performed exceptionally well, with adjusted EBIT of €183.2 million, a significant year-on-year increase, and a profit margin improvement from 3.8% to 6.0%, becoming the core engine of the Group’s profit growth.

Business divergence: The Industrial Vehicles and Services business experienced a short-term decline in profit margins due to sales volume and gross profit structure; the Services business continued its steady growth, supporting overall profitability resilience.

II. Strong order growth across the board, automation business explodes

Growth momentum is the core competitiveness of logistics equipment companies. KION’s order indicators strengthened across the board in 2025, validating the continued recovery in global demand for smart logistics and industrial automation.

New orders for the Group: €11.706 billion, a significant year-on-year increase of 13.4%, significantly outperforming core markets.

Industrial Vehicles & Services: Orders reached €8.147 billion, a year-on-year increase of 4.9%; new vehicle orders totaled 266,000 units, a year-on-year increase of 8.6%, with the proportion of electrified models continuing to rise.

Supply Chain Solutions: Orders reached €3.599 billion, a surge of 39.5% year-on-year, with projects in e-commerce, smart manufacturing, and distribution being implemented intensively, and the automation systems business entering a high-growth phase.

Revenue Growth: Supply Chain Solutions revenue reached €3.071 billion, a year-on-year increase of 4.4%, achieving growth against the trend of a slight decline in overall Group revenue, demonstrating the significant effectiveness of automation transformation.

III. Strong cash flow and secure financial structure

Cash flow and debt levels determine a company’s long-term resilience. KION’s cash flow performance in 2025 exceeded expectations, maintaining an excellent level of financial health within the industry.

Free Cash Flow (FCF): €709.5 million, a slight year-on-year increase, maintaining strong performance for several consecutive years, exceeding market expectations.

Operational Quality: Solid operating cash flow provides strong support for profits, with continuous improvement in project collection and operational efficiency, providing ample “ammunition” for R&D, capacity expansion, and globalization.

Leverage and Debt: A robust leverage ratio based on adjusted EBITDA, a reasonable net debt structure, controllable financing costs, and outstanding counter-cyclical and reinvestment capabilities.

In summary, KION’s 2025 performance delivers three key signals:

- Global demand for logistics equipment has bottomed out and is rebounding, with orders for vehicles and automation systems recovering simultaneously, indicating the industry is entering a new upward cycle.

- Automation solutions are becoming the main growth driver, with brands like Dematic continuing to expand their advantages in warehouse robots, sorting systems, and supply chain scheduling software.

- Servitization + electrification + globalization build long-term barriers, with increased proportions of aftermarket services and high-margin businesses driving continuous improvement in profitability.

Conclusion:

2025 is a year of strategic consolidation and growth accumulation for KION: stable and improved profitability, explosive order growth, and strong cash flow. Amid the global trend of intelligent and green transformation of supply chains, the company continues to solidify its leading global position through a dual-engine structure: its core business in industrial vehicles plus growth from intelligent automation.

For the industry, KION’s robust performance confirms that companies with full-industry-chain capabilities, a global footprint, and technological barriers in automation will be the first to benefit from the new round of industry recovery.