Since the beginning of 2026, the global autonomous driving industry has seen a sustained surge in financing.

On February 24, Zelos closed a new round of financing exceeding $300 million, with a valuation of approximately 10 billion yuan. The following day, UK autonomous driving company Wayve announced a $1.5 billion funding round, pushing its post-funding valuation above $8.6 billion.

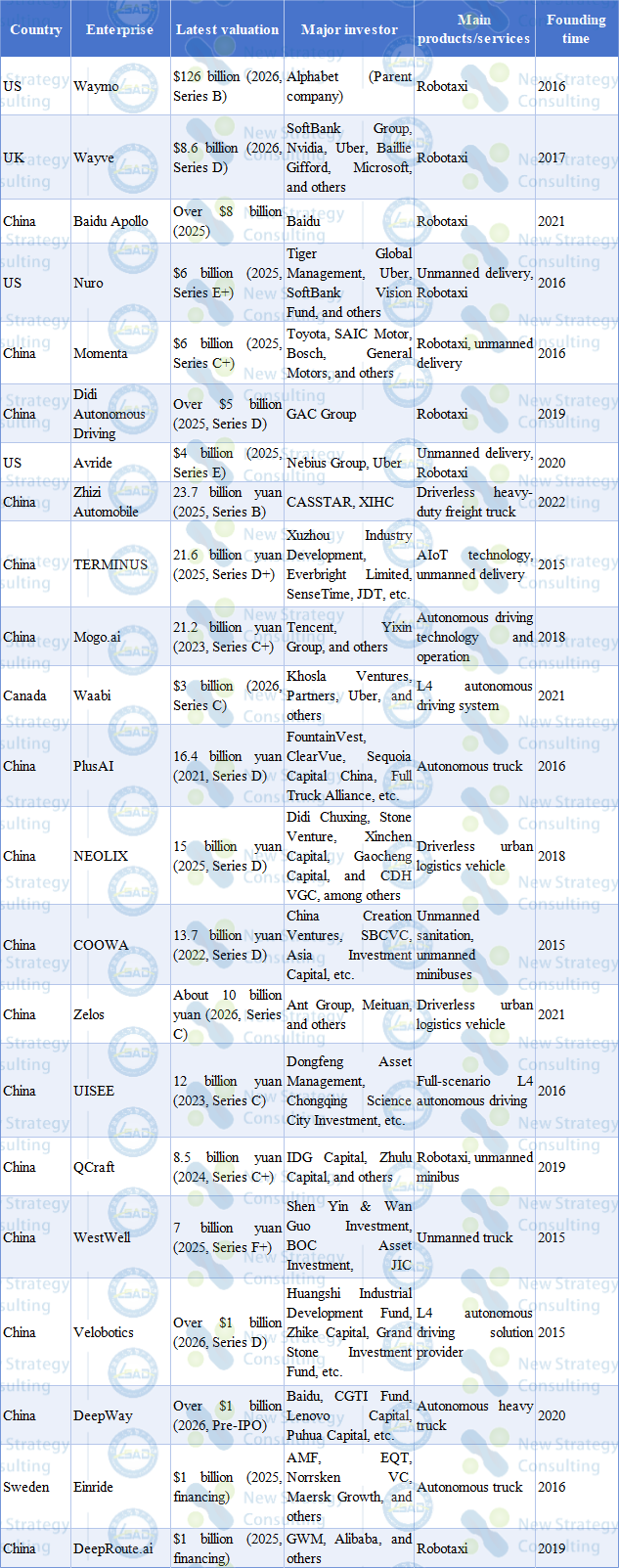

China Low-Speed Automated Driving Industry Alliance (LSAD) observed that multiple large-scale financing deals in the autonomous driving sector, particularly since the start of 2026, have driven significant valuation increases for industry players. According to incomplete statistics from LSAD, as of February 2026, there were 22 autonomous driving companies globally with valuations exceeding $1 billion, including 15 valued over 10 billion yuan and 3 surpassing 50 billion yuan.

Chart: Global Self-Driving Companies with Valuation Exceeding $1 Billion

Among them, Waymo, an American autonomous taxi company, has taken the lead. With a $16 billion funding round completed in early February 2026, the company’s post-investment valuation reached $126 billion (approximately 875.3 billion yuan), more than doubling its $45 billion valuation in October 2024, making it the most expensive unicorn in autonomous driving. Wayve from the UK ranked second with a valuation of $8.6 billion, rapidly rising to become a benchmark in Europe thanks to its end-to-end AI driving model. China’s Baidu Apollo followed closely with a valuation exceeding $8 billion.

In terms of valuation distribution, Waymo stands alone in the $100 billion range, leading the valuation gap, while most companies are concentrated in the multi-billion dollar range, including Wayve, Baidu Apollo, Momenta, Nuro, and NEOLIX, reflecting the concentration of capital in companies with high technological maturity and clear commercialization paths.

From a regional perspective, the global market is dominated by the dual leaders of China and the US, with Europe rapidly catching up. The US holds an advantage in total valuation due to Waymo’s absolute leadership. Besides Waymo, companies like Nuro, Avride, and Waabi are also making continuous efforts in unmanned delivery and L4 systems. China has the most companies, accounting for 16 seats, with NEOLIX, COOWA, Zelos, WestWell, UISEE, and QCraft among others having a combined valuation exceeding $33.5 billion. Covering multiple scenarios such as Robotaxi, unmanned delivery, trunk logistics, and unmanned sanitation, China boasts the most complete ecosystem. Europe is represented by UK’s Wayve and Sweden’s Einride, which have established a foothold in the Robotaxi and autonomous truck sectors through their innovative technologies and solutions.

In terms of sector focus, Robotaxi remains the most capital-intensive field, with Waymo, Wayve, and Baidu Apollo, among the top three in valuation, prioritizing this domain. Notably, over 10 of the 22 listed companies are engaged in Robotaxi operations. Unmanned delivery is another key area attracting investment, with Nuro, NEOLIX, and Zelos specializing in urban logistics, their business models becoming increasingly well-defined. Companies like DeepWay, PlusAI, and Einride target long-haul logistics, achieving commercial closure through reduced labor costs and enhanced efficiency. Additionally, in specialized vertical scenarios such as unmanned sanitation, automated ports, and shuttle services, companies like COOWA, WestWell, and QCraft have carved out differentiated competitive advantages.

Conclusion:

In summary, the high valuation phenomenon in the industry indicates that capital markets remain firmly confident in the implementation of autonomous driving technology and its commercialization cycle, which helps attract massive capital injections, providing sufficient financial support for technological upgrades and large-scale deployment of autonomous driving systems, enhancing corporate risk resilience and expansion capabilities, and accelerating the maturation of the industrial ecosystem.

However, alongside rapid industry expansion, there exists a “bubble risk” concern. Without solid performance support, a market downturn or liquidity tightening could trigger sharp corrections. High valuations imply higher performance expectations. Yet the autonomous driving industry remains in a critical phase of “burning money for the future,” where “high growth, high losses” has become the norm. This mismatch between profit models and valuation expectations will impose significant commercialization pressures on enterprises. Moreover, excessive capital concentration may trigger a “herd effect,” directing resources toward a few leading companies while leaving innovative startups struggling to secure support. Additionally, companies may overinvest in marketing and reckless expansion to maintain high valuation narratives, neglecting core technology development and causing resource misallocation. Therefore, the industry should establish effective risk prevention mechanisms, combining regulatory tolerance with bottom-line thinking to balance capital patience with performance verification, prioritize ecosystem synergy and technological depth, and shift valuation systems from single indicators to multidimensional assessments focusing on non-financial metrics like patent portfolios, data accumulation, and operational efficiency.

Currently, the autonomous driving industry stands at a historical turning point transitioning from “concept validation” to “large-scale commercialization.” High valuations serve as both a prelude to industry boom and a test of corporate wisdom. In the future, companies that can transform capital advantages into technological breakthroughs and turn valuation expectations into closed-loop business models will emerge as winners in this competitive cycle. For the entire industry, maintaining technological resilience amid capital frenzy and preserving business fundamentals during valuation inflation will be the key to navigating economic cycles and achieving sustainable development.