According to public data compiled by the New Strategy Low-Speed Automated Driving Industry Research Institute, China’s low-speed autonomous driving sector maintained strong momentum in the first half of 2026, with over 40 companies launching 44 new vehicle models.

The 44 recorded new models span a diverse range of types, covering key application scenarios such as unmanned sanitation, unmanned delivery, industrial park logistics, smart agriculture, and unmanned mining, which fully demonstrates the comprehensive release of market demand for unmanned operations.

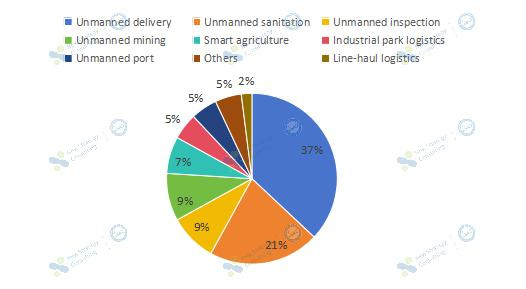

In terms of product categories, RoboVans accounts for the largest share, with approximately 16 new models (over 37% of the total), followed by autonomous sweepers with 8 new models (approximately 21%).

Distribution of New Low-Speed Autonomous Vehicles by Sector in H1 2026

The remaining market share was primarily divided between unmanned inspection and unmanned mining (each at 9%), with the rest comprising new models for smart agriculture, unmanned ports, and industrial park logistics. This distribution confirms that “logistics delivery” and “sanitation/cleaning” sectors with the strongest commercial demand remained the dual core of investment intensity in the low-speed autonomous driving track during the first half of 2026. Competition was fiercest in two areas: completing transport capacity matrices and achieving extreme cost reduction.

Focusing specifically on the unmanned logistics sector, leading domestic companies such as Neolix, Zelos, Dongfeng OpenVAN, Meituan and JDL launched a flurry of new models in the first half of 2026. Notably, Dongfeng OpenVAN released multiple models, including the DF-2, DF-8, DF-25, and DF-60, within a single month. This move highlights the powerful resource integration capabilities and ambitious product matrix strategy of the traditional automaker Dongfeng, in partnership with the tech company Zelos, within the urban unmanned delivery market.

Regarding the vehicle lineup, the new unmanned delivery models feature a distinct tiered distribution in terms of cargo volume and payload capacity, precisely matching logistics needs at various levels. For instance, in the “micro-distance” last-mile delivery segment, models such as the Neolix X1 and Meituan V6 were launched to address the “last 100 meters” challenge, covering scenarios like convenience store restocking, express parcel delivery, and navigation within non-motorized vehicle lanes, while emphasizing compact size, flexibility, and high maneuverability. New models launched in the first half of 2026 for standard urban logistics primarily feature “automotive-grade chassis” and “full-redundancy safety” systems. Examples include the White Rino.ai R24, DST TC50, Zelos Z8 Pro+, and ECAR TECH M6. These models aim to replace traditional internal combustion engine (ICE) light trucks used for urban delivery, serving high-frequency scenarios such as express delivery sorting and supermarket distribution.

In the realm of feeder and heavy-duty logistics, representative models include the Dongfeng OpenVAN DF-8, DF-25, and DF-60. With payloads ranging from 2.8 to 13.6 tons and ranges exceeding 200–300 kilometers, these vehicles are entering markets for inter-city short-haul transport, regional warehouse transfers, and even some long-haul trunk routes, thereby filling the market gap left by autonomous heavy-duty trucks in short-to-medium-distance transport.

Overall, “automotive-grade forward development” has become a major trend for RoboVans. Intelligent algorithms are driving cost reductions and efficiency gains; notably, many new models emphasize independence from high-definition (HD) maps, thereby lowering the costs and complexity associated with cross-regional deployment. Furthermore, breakthroughs in energy replenishment and range such as the adoption of fast-charging technologies have effectively alleviated range anxiety and enhanced the daily fulfillment capacity of individual vehicles.

In the field of unmanned sanitation, new products exhibit distinct characteristics: scenario segmentation, deep technological refinement, and significant efficiency improvements. They demonstrate a clear evolutionary path spanning product iteration, technological upgrades, and commercial implementation:

First, there is comprehensive scenario coverage, ranging from municipal arterial roads and industrial parks/residential communities to underground garages and complex terrains, achieving full penetration across “large, medium, and small” operational environments. For instance, models like Saite Intelligence S1, Gaussian Beetle 2.0, and WeRide’s S3 focus on challenging areas such as residential complexes, back alleys, and urban villages. Models like Gaussian Max-SW, Yushu Intelligent S100, and Jinglv Environment Orca 18 cover large, open, or enclosed spaces. Meanwhile, Yutong’s S5 and WeRide’s multi-functional robosweeper S5 handle deep cleaning on urban arterial roads, reinforcing integrated sweeping and scrubbing capabilities.

Secondly, technical performance has been pushed to the limit: multi-sensor fusion has become standard, enabling centimeter-level positioning and millisecond-level obstacle avoidance; AI models drive efficiency optimization, shifting algorithms from mere “assistance” to “autonomous decision-making”; and hardware breakthroughs have significantly boosted cleaning efficiency.

Furthermore, business models have become clearer; new products tangibly demonstrate “cost reduction and efficiency enhancement,” using data to strengthen their commercial appeal. For instance, WeRide S3 highlights a more than 20% increase in efficiency, while Jinglv Environment Orca 18 boasts an operating area of 6,000–10,000 m² per cycle. By driving progress through the dual engines of cost reduction and efficiency gains, companies are accelerating the sanitation industry’s transition from a labor-intensive model to an unmanned, intelligent one.

New unmanned mining trucks launched in the first half of 2026 are characterized by high-tonnage electrification and full-stack autonomy. Exemplified by Shuanglin’s 248-ton battery-swappable mining truck and Sany’s pure-electric wide-body mining truck, the product lineup has shifted decisively toward heavy-duty loads and new energy. These products address pain points regarding range and flexibility through features like stepless drive-by-wire chassis and rapid five-minute battery swapping. Simultaneously, they emphasize full-stack autonomy; for example, the RTE156 unmanned pure-electric mining truck integrates Boonray’s proprietary L4 autonomous driving system, drive-by-wire chassis redundancy technology, and an intelligent scheduling platform, enabling fully automated loading, transport, and unloading, as well as autonomous obstacle avoidance.

Overall, the new products launched in the first half of 2026 clearly reflect the industry’s transition from the “technology validation” phase to a new stage defined by automotive-grade mass production and large-scale commercial application.

Regarding technical approaches, the adoption of “mapless/light-map” algorithms, end-to-end large models, and automotive-grade fully redundant chassis has emerged as a trend, significantly reducing costs associated with cross-regional deployment and long-term operations and maintenance. In terms of product form, OEMs are deeply involved in driving the evolution from cockpit-less designs to heavy-duty applications, establishing a comprehensive product spectrum ranging from micro to light and heavy-duty vehicles across sectors such as logistics, sanitation, and mining haulage. Commercially, the focus has shifted from mere equipment sales to competition based on transport services centered on total lifecycle costs; combined with breakthroughs in new energy recharging technologies, this shift has realized the economic benefits of unmanned operations in terms of cost reduction and efficiency gains, laying a solid foundation for the large-scale deployment and routine operation of low-speed unmanned vehicles.

To further analyze industry technology trends and build consensus on application scenarios, the 6th Low-Speed Autonomous Driving Scenario Ecosystem Co-construction and Expansion Conference 2026, hosted by the Low-Speed Automated Driving Industry Alliance (LSAD) and organized by Jinglv Environment, will take place in Hefei from July 23 to 24. Industry players from across the entire value chain will gather to conduct in-depth analyses of technical pathways, business models, and future opportunities within the low-speed autonomous driving sector.