Recently, the Hurun Research Institute released the “Global Unicorn Index 2026,” which shows that there are a total of 50 unicorn companies in the robotics sector worldwide. Among them, China leads with 32 companies, followed by the United States with 15, and France, Germany, and Singapore each with one company. These enterprises are primarily concentrated in hardware-driven fields such as humanoid robots and mobile robots, with a combined value of RMB 1.2 trillion.

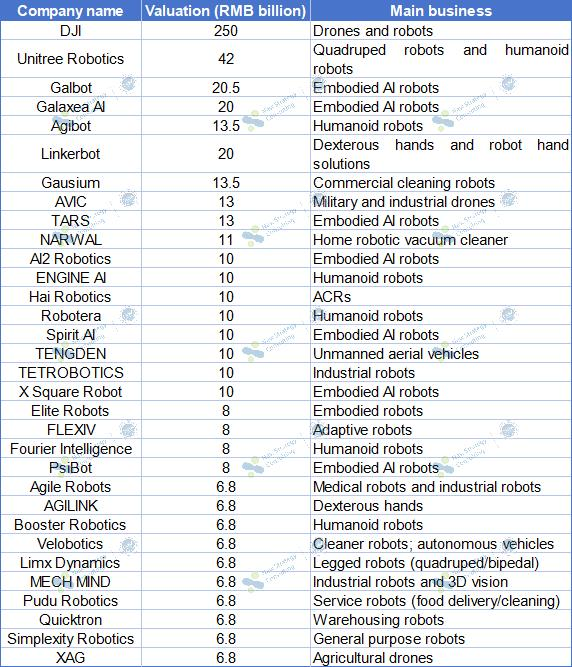

China’s robotics unicorn companies

Source: “Global Unicorn Index 2026” of Hurun Research Institute

The robotics industry is experiencing remarkable diversity, with humanoid robots emerging as the key driver of growth.

The 32 companies featured on this list now extend beyond traditional industrial and logistics robotics, demonstrating a diversified and cutting-edge sector profile. Humanoid/embodied AI robots have emerged as the segment with the highest number of entries, reflecting unprecedented industry interest.

- In the humanoid and embodied intelligence sector,over ten companies—including Unitree Robotics, Agibot, ENGINE AI, Robotera, Limx Dynamics, Booster Robotics, and PsiBot—have made the list. Their product portfolio encompasses general-purpose humanoid robots, legged robots, dexterous hands, and joint components, forming a comprehensive industrial cluster that spans from foundational hardware to mass production of complete systems. Unlike earlier stages focused solely on R&D prototypes, the majority of these humanoid enterprises have achieved small-scale commercialization, with applications in factory handling, commercial services, inspection, and maintenance continuously expanding.

- The industrial intelligent robotics sector continues to expand significantly: MECH MIND specializes in industrial 3D vision sorting; Elite focuses on collaborative robotic arms; while Hai Robotics and Quicktron concentrate on warehousing and logistics robots. These companies comprehensively address the needs of manufacturing automation and smart warehousing upgrades, supporting the wave of intelligent transformation across millions of factories nationwide.

- In the low-altitude drone sector, four industry leaders—DJI, AVIC, TENGDEN, and XAG Technology—collectively form China’s core ecosystem for this field. As the market leader with the highest valuation, DJI covers all application scenarios including consumer aerial photography, industrial surveying, power line inspection, and agricultural operations, while possessing self-developed end-to-end technologies spanning flight control systems, propulsion solutions, and imaging capabilities. AVIC specializes in military-grade and large-scale industrial drones, with a strong focus on long-endurance specialized inspection missions. TENGDEN concentrates on large cargo and emergency rescue unmanned aerial vehicles, whereas XAG is dedicated to agricultural plant protection drones, serving digitalization needs across China’s farmland.

- Home and commercial service robots: NARWAL, Gausium, and Velobotics focus on cleaning robots; Pudu Robotics specializes in food delivery and commercial service robots. Leveraging substantial demand in the consumer market, the company continuously upgrades fully automated cleaning and commercial delivery solutions, aligning closely with daily life needs and ensuring stable commercial revenue streams.

Underlying industrial logic: full-chain autonomy and controllability, with accelerated Chinese substitution.

The inclusion of 32 robotics unicorn companies on the list reflects decades of comprehensive development in China’s robotics industry, with their core strengths manifesting in three key aspects:

First, comprehensive coverage of the entire industrial chain. From upstream components such as precision manipulators, servo motors, and robotic chassis, to midstream products like industrial robotic arms and quadruped humanoid robots, up to downstream applications in warehousing, agriculture, low-altitude operations, and home service terminals, the listed enterprises span all segments of the industrial chain without relying on overseas supply of core components, achieving technological autonomy and controllability.

Second, the vast Chinese market provides fertile ground for experimentation. The extensive applications across Chinese manufacturing, logistics and warehousing, agriculture, commercial services, and the low-altitude economy offer substantial implementation scenarios for robotics companies, enabling rapid product iteration, reduced mass-production costs, and the establishment of a virtuous cycle of “scenario → technology → mass production.”

Third, capital continues to intensify its investment in the embodied intelligence sector. Humanoid robots and general-purpose robots have become key focus areas for venture capital investments, with numerous young talent startup teams and cutting-edge tech companies securing substantial funding to support sustained R&D and innovation, accelerating the transition of Chinese humanoid robots from laboratory prototypes to commercial applications.

The global competitiveness of China’s robotics industry continues to rise.

According to the “Global Unicorn Index 2026”, China significantly outpaces the United States (15 companies) with a numerical advantage of 32 robotics-related unicorns, demonstrating stronger industrial depth across various specialized segments.

However, it must also be noted that quantitative advantages do not equate to comprehensive leadership. In terms of valuation among leading companies, a significant gap remains between China and the United States: Figure AI, an American humanoid robotics company, is valued at RMB 265 billion, whereas Unitree Robotics, China’s highest-valued humanoid robotics company, stands at RMB 42 billion—a difference of over six times. This comparison indicates that China’s robotics industry still has a considerable distance to catch up in terms of core technological barriers and global brand premium capabilities.

Looking ahead, with the continuous decline in the cost of humanoid robots, the gradual implementation of low-altitude economic policies, and the accelerating demand for automation upgrades in manufacturing, the ranks of Chinese robotics unicorns are expected to continue expanding. Meanwhile, leading companies are accelerating their global expansion efforts, leveraging cost-effective products to capture share in the global industrial and service robotics markets. The inclusion of 32 companies on this list marks a new phase for China’s robotics industry, transitioning from following and keeping pace to achieving localized leadership. However, the true golden age of Chinese robotics still awaits as the sector continues to prove its worth through technological innovation and global competition.