The global humanoid robot and embodied intelligence sector remains hot, but capital market activity is becoming more restrained.

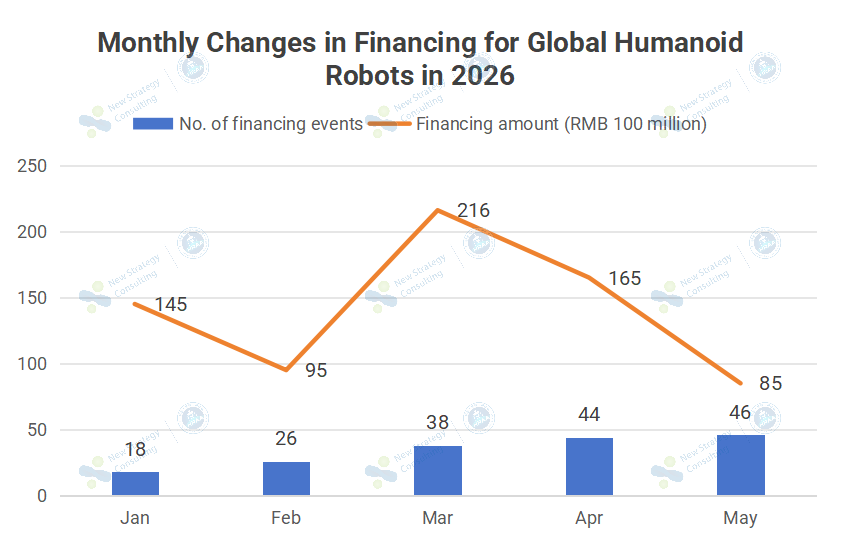

According to incomplete statistics from Humanoid Robot Scene Application Alliance (HRAA), there were over 46 financing events in the global embodied AI and humanoid robot sector in May 2026, with a disclosed total financing amount exceeding RMB 8.5 billion.

In terms of the number of financing events, it continued to grow in May, surpassing 44 events in April and significantly exceeding the levels of each month in the first quarter. This indicates that new companies are still entering the market, and capital’s attention to the sector has not diminished.

However, in terms of the financing amount, a change has emerged. In March, the financing amount in this sector reached RMB 21.6 billion; in April, it dropped to RMB 16.5 billion; and in May, it further decreased to RMB 8.5 billion, marking two consecutive months of decline. In other words, while the number of financing events is increasing, the total monthly amount is falling.

This divergence indicates that the industry is transitioning from “collective warming” to “structural differentiation.”

The pace of financing in the global embodied AI and humanoid robot sector has accelerated significantly this year. As of May 30, 2026, there have been over 172 financing events this year, with a disclosed total financing amount of RMB 70.6 billion, far exceeding the total level of 2025.

A key reason for the rapid increase in the total financing amount is the frequent occurrence of large-scale financing. Since the beginning of this year, there have been more than 28 financing events in this field exceeding RMB 1 billion, with leading companies, star projects, and key component companies receiving concentrated capital investment.

However, in May, while the number of financing events continued to increase, the amount of financing decreased significantly, indicating that more funds are flowing to early-stage projects, with more small and medium-sized financings and a lack of continued concentrated release of large-scale financing. Capital has not left the field; it has simply shifted from “grabbing a position” to “careful selection.”

The underlying reasons are not complicated. While humanoid robots represent a highly certain long-term direction, commercialization is still in its early stages. The industry has moved from prototype demonstrations to scenario pilots, with real demand emerging in areas such as industrial manufacturing, warehousing and logistics, inspection and maintenance, commercial services, and education and research. However, at the same time, product stability, cost control, mass delivery, and scenario adaptability remain hurdles that companies must overcome.

From this perspective, the decline in funding in May does not necessarily indicate a cooling down of the industry. On the contrary, it signals a new phase: the hype remains, but funding is becoming more selective.

Going forward, competition in the humanoid robot industry will shift from “who raises more funding” to “who can deploy their robots faster.” Companies with genuine technological barriers, supply chain capabilities, and application scenarios will continue to receive capital support; players lacking a clear commercialization path may gradually fall behind in the upcoming differentiation.

On June 25, the “3rd Embodied Humanoid Robot Scenario Application Expansion Conference 2026” will be held in Hangzhou, bringing together hundreds of humanoid robot integrators and showcase more than 50 real-world application cases of humanoid robots, helping the industry quickly identify scenario needs and business opportunities, and promoting the transformation of the industry from technological exploration to practical application.

For agenda and registration, please click https://luma.com/qgx5g1em.