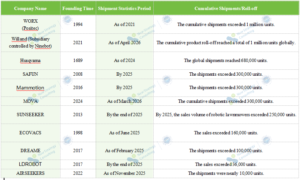

On July 8, EACON officially listed on the Main Board of the Stock Exchange of Hong Kong, becoming the “world’s first listed company dedicated to autonomous driving in mining areas.”

At the opening today, EACON shares traded at HK$91.00, up 3.5% from the offer price of HK$87.92, pushing its total market capitalization past HK$14.1 billion. As of the time of the press time, the trading volume during the opening session stood at approximately 4.46611 million shares with a turnover of about HK$404 million; the stock reached a high of HK$97.00 per share.

The company’s global offering comprised 26,132,000 H-shares priced at HK$87.92 per share, with estimated net proceeds of approximately HK$2.298 billion. Haitong International served as the sole sponsor.

The IPO attracted 11 cornerstone investors who subscribed to a total of approximately 13,011,650 shares, representing about 49.8% of the total offering. These investors included renowned domestic and international institutions such as Zijin Mining, J.P. Morgan, and Barings; cornerstone shares are subject to a six-month lock-up period. The Hong Kong public offering was oversubscribed by approximately 157.82 times, while the international offering saw an oversubscription of about 10.5 times, reflecting strong market enthusiasm.

Over 50% of the net proceeds will be allocated to hardware and software R&D and the iterative upgrade of the “Zhuoshan” autonomous driving system; approximately 23% will be used for business expansion in domestic and overseas mining areas and for global strategic positioning; about 10% will go toward talent acquisition and team building; and the remainder will be used for strategic investments, working capital replenishment, and other general corporate purposes.

Founded in 2018, EACON is a leading provider of L4 autonomous driving solutions for open-pit mining areas in China. Leveraging its proprietary, full-stack “Zhuoshan®” autonomous driving system for closed environments and “Muye®” intelligent control and decision-making platform for mining areas, the company has forged deep partnerships with leading mining groups—such as Zijin Mining and CHN ENERGY—and major mining truck OEMs like Yutong Heavy Industries and TONLY. It focuses primarily on autonomous haulage for open-pit coal and metal mines within closed environments, while gradually expanding into overseas mining sites and scenarios involving diverse mineral types.

Financially, EACON recorded revenues of RMB 271 million, RMB 986 million, and RMB 1.435 billion from 2023 to 2025, representing a compound annual growth rate (CAGR) of 130.2%. Gross margins stood at -18.6%, 7.6%, and 10.1% respectively, marking a turnaround from negative to positive territory and a steady upward trend. Driven by large-scale fleet deployment during a strategic investment phase and significant R&D spending, the company reported a loss for the year of RMB 516 million and an adjusted net loss of RMB 484 million in 2025.

Regarding R&D, expenditures totaled RMB 177 million, RMB 208 million, and RMB 271 million from 2023 to 2025; the R&D expense ratio dropped from 65.4% in 2023 to 18.8% in 2025, with R&D personnel accounting for over 40% of the workforce.

In terms of practical implementation, the company’s solutions have been deployed at nearly half of China’s open-pit coal mines with annual capacities exceeding 10 million tonnes. Its systems have logged over 100 million kilometers of cumulative operation and deployed more than 2,580 autonomous mining trucks globally, all while maintaining a safety record of zero casualties over six consecutive years.

Conclusion:

Over the past year, the pace of capital market activity in the mining-sector autonomous driving space has accelerated significantly.

From the initial public listing of CiDi late last year, to the subsequent IPO filings by BOONRAY and INFINITE MINING, and now the successful listing of EACON on the HKEX, the rapid move of leading players into public markets signals that autonomous mining driving has entered a “golden window” of opportunity backed by capital. This validates the sector’s commercial viability in the eyes of the capital market. Furthermore, as a closed scenario where Return on Investment (ROI) has been successfully proven, the capitalization of mining-sector autonomy is expected to spur investment and financing in other niche areas—such as ports, sanitation services, and last-mile delivery—thereby instilling confidence across the entire low-speed autonomous driving industry.

Indeed, the push toward capitalization and industrial implementation is accelerating across the entire low-speed autonomous driving sector, extending well beyond just mining operations.

With technical validation now a thing of the past and large-scale commercialization widely accepted as the goal, how can we efficiently replicate the successful mining-sector model in other scenarios?

How can capital enthusiasm be precisely translated into growth momentum for the entire industry chain?

Following this wave of IPOs, where will the core of industry competition lie in the next phase?

At this pivotal juncture, the 6th Low-Speed Autonomous Driving Scenario Ecosystem Co-construction and Expansion Conference 2026, hosted by the Low-Speed Automated Driving Industry Alliance (LSAD) and organized by Jinlv Environment, will take place in Hefei from July 23 to 24.

The conference aims to establish a platform for in-depth dialogue between the capital and industrial sectors. By dissecting the commercial logic of mining applications and seeking the “greatest common denominator” for multi-scenario deployment, the event seeks to provide key insights for the high-quality development of the low-speed autonomous driving industry in the post-IPO era.